Who just posted this right-wing market monetarist interpretation of recent events?

Well, the euro area has had a (slightly) shrinking population aged 15-64 since 2008, while the US has not (although our growth is slowing). How does this affect the picture, and what changes?

Europe still does badly, but not by as bad a margin as the raw numbers say:

Photo

CreditAMECO database

Furthermore, the shortfall doesn’t start right away. Things really go off track only in 2011-2012, when the U.S. recovery continues but Europe slides into a second recession. That’s also when the euro area inflation rate slips definitively below target, where the US rate doesn’t to the same degree:

Photo

CreditEurostat, FRED

What was happening in 2011-2012? Europe was doing a lot of austerity. But so, actually, was the U.S., between the expiration of stimulus and cutbacks at the state and local level. The big difference was monetary: the ECB’s utterly wrong-headed interest rate hikes in 2011, and its refusal to do its job as lender of last resort as the debt crisis turned into a liquidity panic, even as the Fed was pursuing aggressive easing.

Policy improved after that, with Mario Draghi’s “whatever it takes” stabilizing bond markets and a leveling off of austerity. But I think you can make the case that the policy errors of 2011-2012 rocked the euro economy back on its heels, pushed inflation down by around a percentage point, and created enduring weakness — because it’s really hard to recover from deflationary mistakes when you’re in a liquidity trap.

Surprisingly, it was Paul Krugman. I’m thrilled, I just wish he’d given us credit for writing lots of posts almost exactly like this one.

And as far as all you Keynesian commenters who complained when I said we’d done as much austerity as Europe, and the real difference was monetary policy, what do you say now?

And all you Keynesian commenters who insisted the ECB could not have offset fiscal austerity because the eurozone was at the zero bound (it wasn’t) what do you say now?

Is Krugman just as clueless as we are?

PS. People sometimes ask me if I’m depressed that I’ve been unable to get the Fed to do NGDPLT. I try to be polite, but My God! We MMs have succeeded beyond our wildest dreams. An increasing number of famous economists favor NGDP targeting. An increasing number of people acknowledge that monetary policy was actually too tight in 2008. The idea that the Fed offset fiscal austerity in 2013 has increasing support. Japan switched policy in 2013, and their CPI is up about 4% (there’s much more work to be done, but previously they were in deflation.) MMs developed the idea of negative IOR, and then major central banks start adopting it. Even better, asset market responses to negative IOR announcement are consistent with MM predictions and inconsistent with the heterodox views you get in the financial press. We predict 2 rate increases in 2016 when the Fed says there’ll be 4, and now the Fed predicts 2. I could go on and on. And remember, within the economics profession we are a bunch of nobodies. If this is failure, I can’t wait for success.

HT: Michael Darda

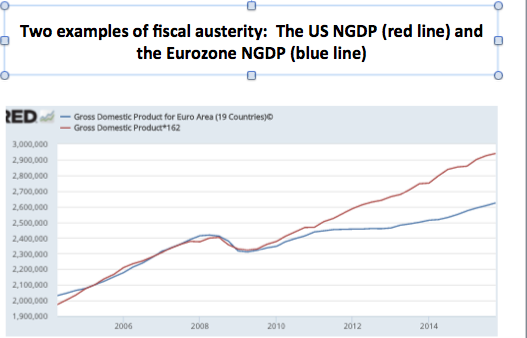

PS. Here’s a screen shot of the PP presentation I’ve been giving for years (I believe I originally got the graph from David Beckworth.)

Yes, this all seemed clear years ago when MMs laid out this case. I wish I could day I was clever enough to discover it on my own. I’ve learned a lot reading this blog.

If one is permitted to attribute changes to the non-targeted variable NGDP as caused by the Fed’s “offsetting”, on the basis that it is a nominal variable, then one is permitted to attribute changes to any non-targeted nominal variable to the Fed’s “offsetting”.

We are not permitted to attribute changes in the spending on, say, the “tuition, healthcare and housing” subset, on the market, because these are nominal variables which the Fed controls, intentionally or not. The Fed by virtue of the offsetting logic, made the spending and prices go up in this subset as an “offset” to the change in spending to “every other expenditure” subset.

And of course THAT latter subset, by the same logic, was also changed by the Fed, because if we now consider the change in spending in the “tuition, healthcare and housing” subset as a given, then the Fed “offset” those changes in the “every other expenditures” subset.

The Fed is in this “offsetting” logic, the cause of changes in any subset of total expenditures, and therefore the cause of the changes to any expenditure whatever, as any expenditure is a subset of total expenditures.

What these graphs show to me is that U.S. policy makers should merely have been fired and replaced long ago. And that Euro policy makers should have been fired and perhaps tarred and feathered to boot.

What they don’t show is a comparison of policy choices between two otherwise similar monetary economies. The difference between a government using the Euro as its currency and the U.S. using the U.S. dollar as its currency is huge. So we see a slow, poor recovery in the U.S. as a result of fairly poor policy choices in a system that would allow for much better (like NGDPLT). And an abysmal failure in much of the Eurozone. But that’s in a monetary union that allows far less flexibility for policy.

As a Keynesian-type commenter, who might have complained about your posts about offsetting austerity in 2013, I am going to say that you long ago convinced me that NGDPLT is a better policy for the Fed or any Central Bank to pursue. But that doesn’t mean that government adopting an appropriate fiscal policy isn’t also important. And I don’t see why you like to say that NGDPLT is a right-wing idea. In my mind right wingers support hard money, zero inflation ideas like returning to a gold standard. I don’t see anything intrinsically conservative about market monetarism. And actually, I don’t see anything really anti-Keynesian about it either. (I mean anti-Keynes as in the guy who wrote that damn book I am still reading because of you. Thank you very much for that.)

I’m impressed Krugman is so honest today. Mario Draghi’s ECB’s monetary policy really has had serious negative effects for Europe and for the rest of the world.

“In my mind right wingers support hard money, zero inflation ideas like returning to a gold standard. I don’t see anything intrinsically conservative about market monetarism.”

Just to comment on one portion though:

“And as far as all you Keynesian commenters who complained when I said we’d done as much austerity as Europe, and the real difference was monetary policy, what do you say now?”

I don’t know if you consider me a “Keynesian commenter” (though you called me “progressive” once, so it’s a possibility). My own answer is the same as I’ve always had: I of course agree with the view that the difference was monetary policy. But why not do both?

Regarding some other comments: MM does have some implications which can be thought of as conservative, especially the opposition to fiscal stimulus, but it’s not a serious matter. An opposition to stimulus need not mean opposition to fiscal policy generally, assuming it meets cost-benefit analyses or other criteria.

Back in 2011 p.k chastised then ecb chairman Jean Claude Trichet for raising rates in order to inpire confidence. Saying that he became victim of the confidence fairy.

My understanding is that p.k had been very consistent advocating for expansionary monetary policy since 08. Why are you and your followers surprised?

I have been reading a collection of Lord Bauer’s essays “From Subsistence to Exchange”. He felt that Economics had both advanced and regressed in his lifetime. He makes the point that dissent needs an echo to have any effect. The great thing about blogging, is that it makes it easier to achieve echoes. The better the blogging, and the better the original ideas and their presentation, the more so.

So, well done. And I have also learned a huge amount from reading this blog; especially due to your generosity about responding to comments.

The national debt is now $19.3 trillion, and the current year deficit, which has been edging up for a couple years now (six years into an economic recovery), is again above $500 billion.

The 21st century has been a non-stop cavalcade of “doing” fiscal policy.

I have a question: to what extent has the Fed policy of paying IOR in excess of the Fed Funds Rate curbed any inflationary tendencies that might otherwise ensued from QE?

Is that even a well-formed question?

The Fed Funds Rate is currently at 0.37%, and IOR is 0.50%.

If the Fed raised the FFR to 0.50% but left the IOR at 0.50%, what would happen? Would this be net contractionary? Would we see the trillions in voluntary reserves go down a lot?

…following up on my previous comment, I’m pretty sure it would be net contractionary. But if banks reduce voluntary reserves, where does the Fed get the money to give to them? Selling assets? Printing?

Sumner: “I try to be polite, but My God! We MMs have succeeded beyond our wildest dreams” – there’s a Monty Python skit on this, involving a arm-less and leg-less knight, who thinks technically he’s not lost the battle.

PS: I bet that when he will finally support NGDPLT (say if Clinton pushed in favor of that idea), Krugman will say something like “it was all in my 1998 paper”.

I know virtually every economist who blogs comments on Krugman, because he has the most readers among economists, but based on the merits of his perspectives, he really should be ignored. He went off the deep end, adopting loonie arguments in favor of mercantilism when in liquidity traps and arguing that raising minimum wages can actually increase demand and employment(when sticky wages are the central problem). I can’t take an economist seriously who says things like that, and I’m a liberal.

“I am going to say that you long ago convinced me that NGDPLT is a better policy for the Fed or any Central Bank to pursue. But that doesn’t mean that government adopting an appropriate fiscal policy isn’t also important.”

Anand –

“My own answer is the same as I’ve always had: I of course agree with the view that the difference was monetary policy. But why not do both?”

These are great comments – I actually think you’re 90% of the way to Market Monetarism. Once you accept monetary offset and that the central bank controls nominal values, you’re almost all the way to accepting that fiscal stimulus is superfluous.

And once you’re there, you realize the only reason to run an annual deficit is to spread out a large one time cost like the Louisiana Purchase or a major war. Otherwise you are just passing taxes for current benefits onto future generations, and diverting investment from private to public resources.

Generally, we should be running surpluses of at least 3% of GDP in most years to pay down debt accumulated during those rare exceptions I mentioned above.

“And as far as all you Keynesian commenters who complained when I said we’d done as much austerity as Europe, and the real difference was monetary policy, what do you say now?”

According to W.M. the real difference was U.S. investment expenditure?

“First, I had been looking for 4% growth for 2013 and scaled back to 2% due to the tax increases and sequesters, and I thought it would continue to weaken until deficit spending increased.

Turns out there was an increase in private sector deficit spending/credit expansion on oil and gas exploration and production that offset the 2013 fiscal adjustments and further expanded in 2014 to further support GDP growth.”

Here’s why Keynesianism almost never applies. In order for fiscal stimulus to work, the monetary authority has to be willing to facilitate it by letting its target variable of choice rise. But, if the monetary authority is willing to do that, why do you need fiscal stimulus? Why needlessly run up debt?

And that is not to mention how clumsily Keynesian spending has been conducted in the past, i.e. too little, too late. Do you really want to depend on Congress manage economic downturns?

As Scott has pointed out, however, it is still possible for supply-side fiscal stimulus to work, as it would raise real growth rather than just inflation. Since sticky wages are the central problem concerning unemployment as a result of nominal shocks, an employer-side payroll tax cut would make it cheaper to hire, boosting real GDP growth and potential.

Fiscal offset would prevent a drop in consumption and investment that would otherwise occur. Otherwise, both the demand and supply of oil would have been lower than would otherwise have occurred, ceteris paribus.

@Negation, great comment. The extent of our fiscal profligacy is even worse when you consider that the Baby Boomer peak earning years are mostly behind us now. That would have been a good time to shore up the government’s finances ahead of the entitlement deluge to come. Oh well.

When I read Dr. Krugman’s post my first thought was that Dr. Sumner had hacked into the NY Times blog site. The real kicker is that Dr. Krugman says he the post was prompted by “doing homework” on the European economy.

@Negation: you said “Generally, we should be running surpluses of at least 3% of GDP in most years to pay down debt accumulated during those rare exceptions I mentioned above.”

Why 3% of GDP Surplus? from the end of WWII to the early 60’s the US did a pretty good job of reducing the massive WWII debt to DGP ratio by simply by running Deficits that weren’t any worse then 3% of GDP.

Capt Parker – You are correct, if debt grows more slowly than NGDP than debt-to-GDP declines (while the debt never gets paid off). However, it would decline faster with surpluses. Also this gives a cushion for emergencies.

[…] of choice for notable centrist Keynesians like Larry Summers. Market monetarists like Scott Sumner, however, continue to argue that negative rates and quantitative easing (via longer-term asset […]

[…] Market monetarists, Keynesians, and some Hayekians have suggested that NGDP targeting would help stabilize an economy. Accordingly, having NGDP grow along its trend should have prevented a major recession in the U.S. and in Europe. Believing in the power of monetary stimulus in times of crisis, these economists criticized the ECB and Fed policy for being too restrictive. They suggest that the ECB should have responded quicker to the evolving crisis and intervened more heavily in markets. The Fed is repeatedly argued to have managed surplus liquidity inadequately. […]

Leave a Reply

Search

About

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Because the distributed lag effect of monetary flows, the proxy for inflation, is 24 months, the FED can tighten N-gDp after two consecutive quarters of greater than 5% growth rates?"

"Because the distributed lag effect of monetary flows, the proxy for inflation, is 24 months, the FED can tighten N-gDp after two consecutive quarters of greater than 5% growth rates?"

"Looking at the one-year rate of change in total reserves you see why stocks and commodities have recently risen. But that is only available since February. I.e., the FED eschews..."

30. April 2016 at 13:42

I guess Dr. Krugman’s wife let him write the column this week.

30. April 2016 at 14:02

Scott,

Yes, this all seemed clear years ago when MMs laid out this case. I wish I could day I was clever enough to discover it on my own. I’ve learned a lot reading this blog.

30. April 2016 at 15:06

Nobodies?

To the king I am a nodody, but to the nobodies I am the king!

Go Market Monetarism!

30. April 2016 at 15:34

If one is permitted to attribute changes to the non-targeted variable NGDP as caused by the Fed’s “offsetting”, on the basis that it is a nominal variable, then one is permitted to attribute changes to any non-targeted nominal variable to the Fed’s “offsetting”.

We are not permitted to attribute changes in the spending on, say, the “tuition, healthcare and housing” subset, on the market, because these are nominal variables which the Fed controls, intentionally or not. The Fed by virtue of the offsetting logic, made the spending and prices go up in this subset as an “offset” to the change in spending to “every other expenditure” subset.

And of course THAT latter subset, by the same logic, was also changed by the Fed, because if we now consider the change in spending in the “tuition, healthcare and housing” subset as a given, then the Fed “offset” those changes in the “every other expenditures” subset.

The Fed is in this “offsetting” logic, the cause of changes in any subset of total expenditures, and therefore the cause of the changes to any expenditure whatever, as any expenditure is a subset of total expenditures.

30. April 2016 at 16:13

What these graphs show to me is that U.S. policy makers should merely have been fired and replaced long ago. And that Euro policy makers should have been fired and perhaps tarred and feathered to boot.

What they don’t show is a comparison of policy choices between two otherwise similar monetary economies. The difference between a government using the Euro as its currency and the U.S. using the U.S. dollar as its currency is huge. So we see a slow, poor recovery in the U.S. as a result of fairly poor policy choices in a system that would allow for much better (like NGDPLT). And an abysmal failure in much of the Eurozone. But that’s in a monetary union that allows far less flexibility for policy.

As a Keynesian-type commenter, who might have complained about your posts about offsetting austerity in 2013, I am going to say that you long ago convinced me that NGDPLT is a better policy for the Fed or any Central Bank to pursue. But that doesn’t mean that government adopting an appropriate fiscal policy isn’t also important. And I don’t see why you like to say that NGDPLT is a right-wing idea. In my mind right wingers support hard money, zero inflation ideas like returning to a gold standard. I don’t see anything intrinsically conservative about market monetarism. And actually, I don’t see anything really anti-Keynesian about it either. (I mean anti-Keynes as in the guy who wrote that damn book I am still reading because of you. Thank you very much for that.)

30. April 2016 at 17:19

I’m impressed Krugman is so honest today. Mario Draghi’s ECB’s monetary policy really has had serious negative effects for Europe and for the rest of the world.

“In my mind right wingers support hard money, zero inflation ideas like returning to a gold standard. I don’t see anything intrinsically conservative about market monetarism.”

-Same thought here.

30. April 2016 at 19:49

I read the piece by Krugman and immediately came here. I actually thought I had opened the wrong blog by mistake, for a bit.

30. April 2016 at 20:08

Just to comment on one portion though:

“And as far as all you Keynesian commenters who complained when I said we’d done as much austerity as Europe, and the real difference was monetary policy, what do you say now?”

I don’t know if you consider me a “Keynesian commenter” (though you called me “progressive” once, so it’s a possibility). My own answer is the same as I’ve always had: I of course agree with the view that the difference was monetary policy. But why not do both?

Regarding some other comments: MM does have some implications which can be thought of as conservative, especially the opposition to fiscal stimulus, but it’s not a serious matter. An opposition to stimulus need not mean opposition to fiscal policy generally, assuming it meets cost-benefit analyses or other criteria.

30. April 2016 at 21:11

Scott

Back in 2011 p.k chastised then ecb chairman Jean Claude Trichet for raising rates in order to inpire confidence. Saying that he became victim of the confidence fairy.

My understanding is that p.k had been very consistent advocating for expansionary monetary policy since 08. Why are you and your followers surprised?

1. May 2016 at 01:13

I have been reading a collection of Lord Bauer’s essays “From Subsistence to Exchange”. He felt that Economics had both advanced and regressed in his lifetime. He makes the point that dissent needs an echo to have any effect. The great thing about blogging, is that it makes it easier to achieve echoes. The better the blogging, and the better the original ideas and their presentation, the more so.

So, well done. And I have also learned a huge amount from reading this blog; especially due to your generosity about responding to comments.

1. May 2016 at 01:14

The collection is available in Kindle form.

http://www.amazon.com/Subsistence-Exchange-Other-Essays-Forum-ebook/dp/B002WJM71C/ref=mt_kindle?_encoding=UTF8&me=

1. May 2016 at 05:08

Very satisfying moment for you, Scott. Well-earned. Bravo!

1. May 2016 at 05:11

@Anand, “But why not do both?”

The national debt is now $19.3 trillion, and the current year deficit, which has been edging up for a couple years now (six years into an economic recovery), is again above $500 billion.

The 21st century has been a non-stop cavalcade of “doing” fiscal policy.

1. May 2016 at 05:20

Scott,

I have a question: to what extent has the Fed policy of paying IOR in excess of the Fed Funds Rate curbed any inflationary tendencies that might otherwise ensued from QE?

Is that even a well-formed question?

The Fed Funds Rate is currently at 0.37%, and IOR is 0.50%.

If the Fed raised the FFR to 0.50% but left the IOR at 0.50%, what would happen? Would this be net contractionary? Would we see the trillions in voluntary reserves go down a lot?

1. May 2016 at 05:25

…following up on my previous comment, I’m pretty sure it would be net contractionary. But if banks reduce voluntary reserves, where does the Fed get the money to give to them? Selling assets? Printing?

Maybe I’m thinking about IOR wrong.

1. May 2016 at 05:26

Everyone, Thanks for the support.

Jerry, You said:

“And I don’t see why you like to say that NGDPLT is a right-wing idea.”

I never said it was.

Anand, You said:

“An opposition to stimulus need not mean opposition to fiscal policy generally, assuming it meets cost-benefit analyses or other criteria.”

But that’s not what economists mean by the term “fiscal policy”

James, For years Krugman was saying that austerity caused the double dip recession in Europe. Now he says (quite correctly) it was tight money.

This is the story I’ve been telling for years, and I’ve been criticized by one Keynesian after another.

1. May 2016 at 07:10

Sumner: “I try to be polite, but My God! We MMs have succeeded beyond our wildest dreams” – there’s a Monty Python skit on this, involving a arm-less and leg-less knight, who thinks technically he’s not lost the battle.

1. May 2016 at 07:17

Bravo.

PS: I bet that when he will finally support NGDPLT (say if Clinton pushed in favor of that idea), Krugman will say something like “it was all in my 1998 paper”.

1. May 2016 at 10:26

I know virtually every economist who blogs comments on Krugman, because he has the most readers among economists, but based on the merits of his perspectives, he really should be ignored. He went off the deep end, adopting loonie arguments in favor of mercantilism when in liquidity traps and arguing that raising minimum wages can actually increase demand and employment(when sticky wages are the central problem). I can’t take an economist seriously who says things like that, and I’m a liberal.

1. May 2016 at 10:33

Jerry –

“I am going to say that you long ago convinced me that NGDPLT is a better policy for the Fed or any Central Bank to pursue. But that doesn’t mean that government adopting an appropriate fiscal policy isn’t also important.”

Anand –

“My own answer is the same as I’ve always had: I of course agree with the view that the difference was monetary policy. But why not do both?”

These are great comments – I actually think you’re 90% of the way to Market Monetarism. Once you accept monetary offset and that the central bank controls nominal values, you’re almost all the way to accepting that fiscal stimulus is superfluous.

And once you’re there, you realize the only reason to run an annual deficit is to spread out a large one time cost like the Louisiana Purchase or a major war. Otherwise you are just passing taxes for current benefits onto future generations, and diverting investment from private to public resources.

Generally, we should be running surpluses of at least 3% of GDP in most years to pay down debt accumulated during those rare exceptions I mentioned above.

1. May 2016 at 10:43

“And as far as all you Keynesian commenters who complained when I said we’d done as much austerity as Europe, and the real difference was monetary policy, what do you say now?”

According to W.M. the real difference was U.S. investment expenditure?

“First, I had been looking for 4% growth for 2013 and scaled back to 2% due to the tax increases and sequesters, and I thought it would continue to weaken until deficit spending increased.

Turns out there was an increase in private sector deficit spending/credit expansion on oil and gas exploration and production that offset the 2013 fiscal adjustments and further expanded in 2014 to further support GDP growth.”

http://econlog.econlib.org/archives/2015/01/the_keynesian_s.html

1. May 2016 at 12:13

Jerry Brown,

Here’s why Keynesianism almost never applies. In order for fiscal stimulus to work, the monetary authority has to be willing to facilitate it by letting its target variable of choice rise. But, if the monetary authority is willing to do that, why do you need fiscal stimulus? Why needlessly run up debt?

And that is not to mention how clumsily Keynesian spending has been conducted in the past, i.e. too little, too late. Do you really want to depend on Congress manage economic downturns?

1. May 2016 at 12:16

As Scott has pointed out, however, it is still possible for supply-side fiscal stimulus to work, as it would raise real growth rather than just inflation. Since sticky wages are the central problem concerning unemployment as a result of nominal shocks, an employer-side payroll tax cut would make it cheaper to hire, boosting real GDP growth and potential.

1. May 2016 at 12:19

Postkey,

Fiscal offset would prevent a drop in consumption and investment that would otherwise occur. Otherwise, both the demand and supply of oil would have been lower than would otherwise have occurred, ceteris paribus.

2. May 2016 at 03:58

@Negation, great comment. The extent of our fiscal profligacy is even worse when you consider that the Baby Boomer peak earning years are mostly behind us now. That would have been a good time to shore up the government’s finances ahead of the entitlement deluge to come. Oh well.

2. May 2016 at 07:08

When I read Dr. Krugman’s post my first thought was that Dr. Sumner had hacked into the NY Times blog site. The real kicker is that Dr. Krugman says he the post was prompted by “doing homework” on the European economy.

@Negation: you said “Generally, we should be running surpluses of at least 3% of GDP in most years to pay down debt accumulated during those rare exceptions I mentioned above.”

Why 3% of GDP Surplus? from the end of WWII to the early 60’s the US did a pretty good job of reducing the massive WWII debt to DGP ratio by simply by running Deficits that weren’t any worse then 3% of GDP.

2. May 2016 at 07:46

“The Legacy of Joan Robinson”

http://econospeak.blogspot.com/2016/05/the-legacy-of-joan-robinson.html

2. May 2016 at 07:48

Pethokoukis: “Why US productivity growth may be ready for a rebound”

http://www.aei.org/publication/why-us-productivity-growth-may-be-ready-for-a-rebound

2. May 2016 at 15:48

LK, He did sort of endorse NGDP targeting, back around 2011 or 2012.

3. May 2016 at 03:39

Thanks Brian!

Capt Parker – You are correct, if debt grows more slowly than NGDP than debt-to-GDP declines (while the debt never gets paid off). However, it would decline faster with surpluses. Also this gives a cushion for emergencies.

9. May 2016 at 14:23

[…] of choice for notable centrist Keynesians like Larry Summers. Market monetarists like Scott Sumner, however, continue to argue that negative rates and quantitative easing (via longer-term asset […]

15. August 2018 at 02:29

[…] Market monetarists, Keynesians, and some Hayekians have suggested that NGDP targeting would help stabilize an economy. Accordingly, having NGDP grow along its trend should have prevented a major recession in the U.S. and in Europe. Believing in the power of monetary stimulus in times of crisis, these economists criticized the ECB and Fed policy for being too restrictive. They suggest that the ECB should have responded quicker to the evolving crisis and intervened more heavily in markets. The Fed is repeatedly argued to have managed surplus liquidity inadequately. […]