Sloppy thinking at The Telegraph (plus, I was wrong about Abenomics)

Today I’ll dissect a really sloppy article in The Telegraph:

To paraphrase Senator Everett Dirksen’s famous quote on the American military budget: a trillion here, a trillion there, and pretty soon you are talking about real money. Central banks may not have that much in common with the Army, but they are starting to fall into the same habit of spraying vast quantities of money at a problem, despite a troubling lack of evidence that it has any real impact.

Last week, the European Central Bank president Mario Draghi extended his quantitative easing programme, and drove interest rates even deeper into negative territory. And yet, despite the billion of euros printed, inflation across the eurozone resolutely refuses to pick up.

Central banks don’t spend money in the fiscal sense; they create money and swap it for other assets.

So the ECB adopts a tight money policy in 2011 and the eurozone goes into recession. Draghi then switches to a slightly more expansionary policy in 2013 and the economy begins to recover. But because inflation is temporarily depressed by plunging imported oil prices, this somehow shows monetary policy is ineffective? I don’t get it.

Here in the UK, the Bank of England is meant to generate price rises of 2pc a year, but Chelsea FC are hitting the back of the net more frequently this season than the Bank hits its inflation target. Likewise in Japan and the US, central banks are consistently missing their official targets for inflation. What is going on?

So exactly how badly are the central banks missing their targets? By 10%? By 5%? By 1%? It does make a difference, no one expected perfection. After all, they were often 1% or 2% off during the Great Moderation.

Up until 2013 the BOJ was not trying to create inflation. Then they adopted a 2% inflation target. Here’s what happened:

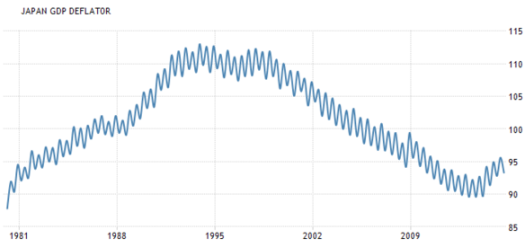

Over the past two years Japan has moved from a trend rate of 1% annual deflation to 2% annual inflation, using the GDP deflator. (I wish they’d give us seasonalized data.) That seems like a huge success to me. What am I missing?

Over the past two years Japan has moved from a trend rate of 1% annual deflation to 2% annual inflation, using the GDP deflator. (I wish they’d give us seasonalized data.) That seems like a huge success to me. What am I missing?

But what about unemployment? Oh yeah, that just fell to the lowest rate since the golden days of the early 1990s:

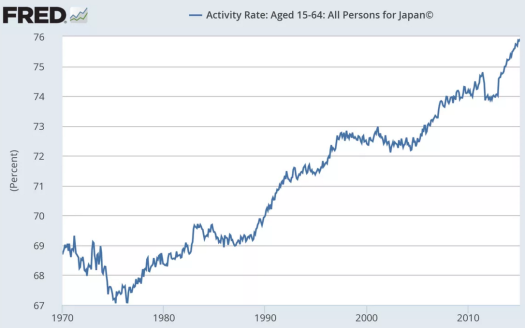

So they’ve hit their inflation target, and had huge success in lowering the unemployment rate. But isn’t that achieved by people exiting the labor force? Nope, just the opposite, Matt Yglesias recently pointed out that labor force participation in Japan is high and rising under Abenomics:

But what about the CPI? Yes, CPI inflation has been depressed recently by imported oil prices. That’s why the GDP deflator is a better indicator; it’s the price of domestically made goods matters for macroeconomic stability. (Obviously I’d prefer NGDP.)

But what about the CPI? Yes, CPI inflation has been depressed recently by imported oil prices. That’s why the GDP deflator is a better indicator; it’s the price of domestically made goods matters for macroeconomic stability. (Obviously I’d prefer NGDP.)

So Japan’s hit almost exactly 2% inflation on Japanese produced goods and services, after decades of steady 1% deflation. Unemployment has fallen to a multi-decade low. Labor force participation is soaring. And yet we are to believe that Abenomics has failed solely because Japanese motorists are suffering from dramatically cheaper imported oil, and as a result Japanese real wages are rising strongly? This stuff is so silly I couldn’t make it up if I tried. Whenever I read someone suggest that Abenomics has failed I immediately write them off as non-serious.

I was wrong about Abenomics. I thought the monetary “arrow” would be a modest success, as they were on the right track but not doing enough. In fact, so far the monetary arrow has been an overwhelming success, beyond almost anyone’s wildest dreams. (The other two arrows are still in the quiver.) I’m still expecting closer to 1% inflation over the next few years, but even that would be a huge success compared to recent decades.

But how about the US? Haven’t we fallen short of 2%? Yes, but the Fed is about to raise interest rates next week precisely because they think inflation is only temporarily depressed by falling oil prices, and that we are on track to 2% inflation when that shock passes. (Yes, oil prices are still falling, but surely they can’t fall below zero.)

I suspect the Fed is too optimistic, but this has nothing to do with the impotence of monetary policy. Even economists who think QE is 100% ineffective concede the Fed could choose to not raise interest rates in December, and that this would lead to higher inflation. You might not like Fed policy, but the Fed believes inflation is right on track to being on target in a couple years. I thought the silly blather about monetary policy ineffectiveness would stop once the Fed raised rates, but that doesn’t seem to be the case.

A new paper by the Bruegel Institute argues that central banks have lost their ability to control inflation. At the moment, that doesn’t matter very much, because prices are generally stable. But (and it’s a big “but”) if we can’t control inflation on the way down – and it appears we can’t – what makes us think we can control it on the way up? Once prices do finally tick up, it may turn out to be impossible to stop them. And that is worrying.

By now it should be clear to everyone that the ability of central banks to control inflation has disappeared. Take the eurozone to start with. The ECB has an official target of prices rising by 2pc a year.

Clear to everyone? First one needs to present some evidence, and the author fails to do so. He also gets the ECB’s inflation target wrong; it’s not 2%, it’s “below but close to 2%”. Yes, the inflation rate is further below 2% than they’d like, but that partly due to the recent plunge in oil prices. And why would central banks be unable to prevent rising inflation? None of the theories that I know of that predict monetary policy impotence at the zero bound have any implication for preventing a rise in inflation.

Then again, it may be something more serious. In a recent paper for the Bruegel Institute, Gregory Claeys and Guntram Woolfe argue that central banks may have lost their ability to control inflation. They point out that globalisation and new technologies have already been shown to have had a powerful disinflationary impact right around the world: “The important question is whether these integration trends affect the transmission mechanisms of monetary policy and reduce the ability of central banks to fulfill their mandate.”

This isn’t just wrong, it’s doubly wrong. Positive supply shocks don’t prevent central banks from hitting their inflation target. Not in monetarist models. Not in New Keynesian models. Not in Austrian models. Not in any plausible fiat money model. Even worse, to the extent that positive supply shocks hold down inflation, they do so by boosting output growth. But growth has also been unusually low in recent years, not just in the US, but also globally. Fast rising productivity due to globalization is the least of the world’s problems.

PS. I have a post on Krugman/Cruz over at Econlog.

HT: Caroline Baum

Tags:

8. December 2015 at 11:41

Great post, Scott.

8. December 2015 at 13:33

BoE are ahead of their target because our inflation figures don’t reflect housing costs which are up nearly 10%.

They can control both the inflation figure you look at in a spreadsheet and the actual inflation figure on the ground for working people.

But as usual what they refuse to do is to foster wealth creation at the expense of spreadsheet figures looking bad.

8. December 2015 at 15:45

@ Ben:

What’s this baloney about “spreadsheet inflation”? On a spreadsheet you can represent any measure of inflation you like, including “actual inflation on the ground for working people” (whatever that is!).

8. December 2015 at 16:26

Excellent blog in, and I agree with 99% of this post.

I do think globalization has played a role in inflation, a positive reducing role. For example, in the United States auto prices have not changed in 20 years, despite a doubling of sales in the last 7 years. In past eras, you might have seen the Big Three and the UAW extract price hikes.

What this tells me is that globalization has decreased inflation, and that all central banks should be pursuing aggressive growth-oriented policies. For the Federal Reserve, it means a field is wide open to put the pedal to the metal.

About the only inflation we will see in the US is from housing, and that is controlled by supply constraints at the local level. There is nothing we can do about that. Nobody wants a high-rise condo with retail ground-floor activity in their single-family detached neighborhood.

8. December 2015 at 16:27

Add on: I have been saying that Haruhiko Kuroda is the world’s best central banker, and I am glad to see others are coming in to my point of view.

8. December 2015 at 16:31

The inflation figures in the UK are a lie. They exclude housing to allow printing via land. This guy just takes the figure at face value.

8. December 2015 at 17:33

Japan is set for another crash.

Yay monetarists.

8. December 2015 at 20:49

Sumner: ‘what am I missing?’. Answer: (Google News) “Japan’s economy crawled out of recession in the fourth quarter of 2014, data on Monday showed, although the growth figures came in much weaker than expected.” Success says Sumner!

The only thing I found interesting was the seasonality of Japan’s inflation. Apparently the year-end holiday gift giving custom really distorts their inflation.

@Benjamin Cole: “Nobody wants a high-rise condo with retail ground-floor activity in their single-family detached neighborhood” – lol! Spoken by a true tyro who has probably never owned real estate in their life. First off, few developers would build in the middle of a low-density residential neighborhood a high-rise condo, as likely buyers would not want to live there, but, should any such developer do so, I would love to be right next door to them: the real estate land values surrounding the high-rise would skyrocket, as anybody who has speculated in real estate, like I do, would know. But thanks for your opinion.

8. December 2015 at 22:24

Ray Woepez:

I have owned M1 and R3 land in Los Angeles, and farmland in Thailand. Done quite well— for various wives and lawyers. Still have the farmland on long-term lease.

Stop being such a little snot and pay a visit if you like.

9. December 2015 at 04:55

Hi, Scott. A huge fan here and an avid reader since 2011. Thanks always for your fantastic posts.

A bit disappointed that I can’t share a stark chart through this, but wanted to share some more encouraging facts on Japan’s adoption of firm nominal target.

General account tax revenue (4Q rolling sum) as % of NGDP

2012 Q4: 9.08%

2015 Q3: 11.25% (20 year average = 9.5%)

General government financial deficit (Q4 rolling sum) as % of NGDP

(From flow of funds data)

2012 Q4: 8.56%

2015 Q3: 3.86%

Abenomics works.

9. December 2015 at 05:33

@Benjamin Cole – my apologies. Having lived a year in Thailand I understand your plight; I stand corrected. Anyway, land is constantly in short supply in prime locations, that’s why the people who own prime land were considered by economist Henry George as rent seekers who should be taxed extra heavy. But I hope you don’t believe Kevin Erdmann’s crackpot thesis that there was no real estate bubble. That’s as delusional as a belief that monetarism has more than just 3.2% to 13.2% effect on economic variables.

9. December 2015 at 05:51

[…] Sumner on the smashing success of Japanese monetary expansion. […]

9. December 2015 at 06:05

Ray Woepez: I believe a different crackpot theory…I believe there was a reverse real estate bubble 2009 to 2010.

9. December 2015 at 06:45

Prof. Sumner,

Thought you might be interested in this piece from the FT: http://www.ft.com/intl/cms/s/0/23232c52-9a7d-11e5-a5c1-ca5db4add713.html#axzz3tfK72P9C

Tighter policy means lower rates–sounds familiar. That forecast of 1.5 for the 10-year by the end of next year is astounding.

9. December 2015 at 07:27

Another flawed analysis that CNBC says is hugely popular on Wall Street:

http://www.businessinsider.com/a-wall-street-ceo-perfectly-explained-the-hot-theory-for-the-economy-markets-and-everything-2015-12

“The idea here is that technological advancements help drive prices down, whether it’s through lowering the cost of production (think manufacturing), accessing new resources (think shale) or increasing price transparency (think Amazon).

…….

It is a really big picture idea, but it’s gaining traction with people on Wall Street. We’ve heard a number of people bring it up now.”

Durrrrr

9. December 2015 at 07:31

“There is one force reshaping the entire world ― and Wall Street is catching on”

http://www.businessinsider.com/technological-deflation-could-be-the-answer-to-economy-2015-12

Durrrrr

9. December 2015 at 09:17

Thanks Brian,

Ben, Looks like you were right about Kuroda

Ray, You mean you haven’t read any of my posts on the phony Japanese “recessions”, which occur despite falling unemployment? Or do you just have a very bad memory?

HL< Thanks, that's very interesting. Do you have a link to the site? Anonymous, Yes, interesting article. Travis. I like how they present positive supply shocks as a "new theory" and then fail to account for slowing RGDP growth.

9. December 2015 at 12:19

“crazy theory that the tulip bubble wasn’t actually a bubble”

http://www.businessinsider.com/craig-steven-wright-alleged-bitcoin-founders-theory-on-tulip-mania-bubble-2015-12

9. December 2015 at 12:56

TravisV, I can tell you the “dot com bubble” was NOT a bubble, it was a crapshoot with very high upside.

9. December 2015 at 15:01

I told you so…

9. December 2015 at 18:29

Off-topic, but Mises on Sumner’s belief in inevitable progress:

“To disprove this doctrine of an inherent tendency toward progress that operates automatically, as it were, there is no need to refer to those older civilizations in which periods of material improvement were followed by periods of material decay or by periods of standstill. There is no reason whatever to assume that a law of historical evolution operates necessarily toward the improvement of material conditions or that trends which prevailed in the recent past will go on in the future too. What is called economic progress is the effect of an accumulation of capital goods exceeding the increase in population. If this trend gives way to a standstill in the further accumulation of capital or to capital decumulation, there will no longer be progress in this sense of the term.

“Everyone but the most bigoted socialists agrees that the unprecedented improvement in economic conditions which has occurred in the last two hundred years is an achievement of capitalism. It is, to say the least, premature to assume that the tendency toward progressive economic improvement will continue under a different economic organization of society.”

Shoulda posted it when Sumner posted on this topic at EconLog a few months ago. I should read more Mises.

9. December 2015 at 19:27

@Sumner – yes, now I remember, you did blog on Japan being richer despite technical ‘recession’. The problem with this type logic is the people getting richer in this environment are not the young, who need jobs, but the older people who are often rich and have capital.

@E. Harding – Mises was living in a time when population was growing and the frontier economies had not stagnated. So he confused growth with capitalism. But you can have no-growth with capitalism (think about the capitalist Italian city-states after the India spice trade was stopped when the Spanish and Portuguese discovered new trade routes; the IT city-states died out; also see China today and the USSR during WWII, which grew nicely, albeit by copying technology from the leading frontier countries in the West).

10. December 2015 at 07:34

Hi, Scott

The charts are mine (from my work as a macro guy at a financial firm).

Government’s financial balance as % of GDP

https://twitter.com/Luxury_Duck/status/674973163713761284

Government’s general account tax revenue as % of GDP

https://twitter.com/Luxury_Duck/status/674974976764567553

10. December 2015 at 07:37

Sorry the link was wrong. Posting again.

Government’s general account tax revenue as % of GDP

https://twitter.com/Luxury_Duck/status/674975976321748992

10. December 2015 at 09:41

More evidence that perhaps very low inflation (below 2%) or NGDP growth sacrifices real growth/employment in modern economies, for reasons perhaps not limited to sticky wages.

There’s a lot of insistence that inflation cannot create growth, which is true in a general sense, but there seems to be some strong empirical relationship here, such that there is some ideal level of inflation or NGDP growth which could maximize employment/RGDP, and should be targeted.

Hopefully the dollar and euro economies will experience a similar result.

10. December 2015 at 11:31

Ok, so who gets credit for the decline in UE from 2009-2013? Under deflation according to these graphs? Who gets the blame for rising UE from 1981-1988 under inflation?

http://sebwassl.blogspot.com/2015/12/two-graphs-presented-by-scott-sumner.html

10. December 2015 at 17:28

Travis, Thanks, another bubble theory popped.

Lars, Yes, you were right.

E. Harding, You said:

“Sumner’s belief in inevitable progress”

You are wasting your time, I don’t believe that progress is inevitable. I think it’s not that unlikely that we destroy ourselves.

Ray, Can’t you read? The young are getting jobs.

Bacon, For your first question, how about the natural rate hypothesis? And for your second, how about a rise in the natural rate of unemployment?

10. December 2015 at 19:30

@Sumner – I was referring to the known phenomena in Japan of elderly savings doing well under the “Lost Decades” economic environment; the youth, not so much.

OT – real “concrete steps”, not metaphysics. German economist List also advocated industrial policy. Patents (which I favor) are one such policy. Danger is that infant industries rarely grow up, and regulatory capture. Sumner should blog on this.

Amazon.com –

Concrete Economics: The Hamilton Approach to Economic Growth and Policy Kindle Edition

by Stephen S. Cohen (Author), J. Bradford DeLong (Author)

Brilliantly written and argued, Concrete Economics shows exactly how the US government has shaped and directed the economy since the very inception of the country.

This book does not rehash the sturdy and well-known arguments that to thrive, an entrepreneurial economy needs a social and policy environment characterized by a broad range of freedoms. Nor does it buy into the myth of the absolutely free market.

Instead, Cohen and DeLong focus on the forgotten role played by the US government in initiating and enabling a redesign of the US economy. The government not only sets the ground rules for entrepreneurial activity but directs the surges of energy that mark a vibrant economy. It is as true for present-day Silicon Valley as it was for New England manufacturing at the dawn of the nineteenth century.

11. December 2015 at 07:47

Concerning the tulip bubble, the article TravisV linked does not dispute that tulips increased in price far above their fundamental value. What is offered is the opinion that the collapse in price was triggered by a change in the law. This may be so and yet it does not change the reality of a frenzied speculation in tulips. Are we to suppose that if the law was not changed that the elevated price of tulips would have continued indefinitely?

At issue is not that the price of tulips went up or that they went down. The issue with speculative manias is when such price changes involve levered investments and the downward price change forces liquidation of capital held by politically influential people.

11. December 2015 at 08:16

“Bacon, For your first question, how about the natural rate hypothesis? And for your second, how about a rise in the natural rate of unemployment?”

Isn’t this exactly what you have criticized Krugman for? That “other factors” are important when the model doesn’t fit the data?

According to what I have read of your writing I can only surmise that you classify the period from 2010-2013 in Japan as “tight money”- and not just tight money like in the US where they are getting inflation failing to achieve the inflation target, but tight money to the extent of deflation. If Japan had no inflation target in 2010 and just was targeting UE (a measure you have suggest is most important for determining economic health)- why should they have changed strategies in 2013?

11. December 2015 at 08:43

Bacon, You said:

“Isn’t this exactly what you have criticized Krugman for? That “other factors” are important when the model doesn’t fit the data?”

Whoa, you have totally misunderstood “the model.” The natural rate hypothesis is very much a part of the MM model. Japan was in deflation for almost 20 years, it’s no surprise that the wage rate would EVENTUALLY adjust to the falling prices. Indeed if unemployment had not fallen I’d be more inclined to worry about the model.

As far as the 1980s, the Japanese unemployment rate fluctuated between 2% and 3% during the entire decade, lower than today. Please tell me how that is at odds with the MM model.

Also, your comment mentioned inflation and deflation, but not NGDP growth, and yet the MM model says NGDP growth matters but not inflation. So that makes me wonder whether you even understand the MM model. I’d encourage you to go back and read my posts on the Musical Chairs model. And then get some data for NGDP growth.

Let’s say I’m wrong about Japan. What sort of NGDP deflator and unemployment and labor force participation and budget deficit number would you have suggested constituted “success” when Abenomics was first implemented? What would you have looked for as an indicator of success?

11. December 2015 at 18:35

What about Russia?

17. December 2015 at 00:15

I’ve heard of situations where central banks lose control of the money supply, but I’ve never heard of them losing control over inflation. I suppose it’s plausible a central bank could lose control for a few years once every few centuries, or something like that, but not on a permanent, on-going basis.

The Fed maintained it’s target throughout the 90s productivity shock, didn’t it? Seems like a strange argument to make.

17. December 2015 at 00:25

From the article:

“For long-term rates, this is less clear [that central banks can control them], however. The conundrum episode of 2004-06 in the US (see Figure 3) suggests that long-term rates can become less sensitive to short-term rates and that external factors can affect them significantly.”

Isn’t that what “macro-prudential” policy is supposed to be for? To allow the Fed to tighten credit the next time it loses control over long-term rates? Or am I misunderstanding that?

30. December 2015 at 03:36

[…] Japan avoids a recession, Scott Sumner is declaring Abenomics a success against his […]

26. January 2016 at 01:16

[…] Japan avoids a recession, Scott Sumner is declaring Abenomics a success against his […]