Money and Inflation, Pt. 1 (The long twilight of gold)

In a previous post I argued that money is important because it pins down nominal variables like the price level and NGDP. In this post and the next couple, I’ll explain how money determines the price level. Let’s start with the most common monetary system in modern world history—the silver standard. Indeed let’s assume that the unit of account is one pound of sterling silver, or “pound sterling” for short. Silver itself is the medium of account.

Money can be defined in many ways, including the medium of account, the medium of exchange, or highly liquid assets. I believe the medium of account definition is the most useful, as it will allow us to quickly zero in on the key issues, without the distractions of media of exchange that might or might not be convertible into silver.

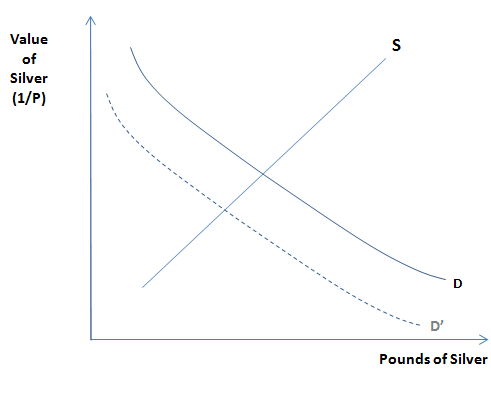

As noted earlier, the value of the medium of account (let’s call it “money”) is equal to 1/P. The price level is determined in the silver market. Modeling the (long run) price level is a microeconomic problem. However the various effects of changes in the price level are macroeconomic problems. Here’s how simple it is to model the (long run) price level when silver is money:

When there is a new silver discovery that shifts the supply of silver to the right, the value of silver falls and the price level rises inversely proportionately to the fall in the value of money—by definition. There is no quantity theory of money yet; that will come later with fiat money (although ironically the theory was invented during a commodity money period where it doesn’t quite apply.)

Eventually most nations switched onto a gold standard regime; in the US the unit of account was the dollar, defined as 1/20.67 ounces of gold (until 1933.) Because governments generally don’t operate gold mines, monetary policy consists of one tool, and one tool only, shifts in the demand for gold. This can be done in all sorts of ways, such as changing the amount of gold backing each paper dollar via OMOs or discount loans, or by changing reserve requirements so that banks demand more currency, which leads to a greater derived demand for gold to back that currency. Less demand for gold was expansionary (shown on graph), and vice versa. Small countries obviously had little impact on the value of gold, which was determined in global markets.

Under a gold standard there was a “zero lower bound problem” for gold reserves, which Keynes misdiagnosed as a liquidity trap. Thus it’s easier to do tight money than easy money, because easy money is constrained by the fact that central bank gold demand (gold reserves) cannot fall below zero.

Most people think this is why the US left the gold standard in 1933. However we didn’t really leave the gold standard, we just temporarily suspended it, and we were never even close to running out of gold reserves. It’s not clear what the real problem was—perhaps FDR couldn’t get the Fed to inflate as much as he wished, and thus did an end run by raising the price of gold. Even so, the dollar was re-fixed to gold in 1934, and stayed fixed until 1968, when we finally stopped using gold as a medium of account.

The long phase-out of gold lasted for 34 years, and saw a very large rise in the price level. This inflation can be attributed to three factors, two of which reflected decisions of FDR, and the third was luck:

1. The revaluation of gold from $20.67 per ounce to $35/oz. This alone raised prices by 69%.

2. FDR reduced global gold demand by making it illegal for Americans to hoard gold. Later American presidents reduced the gold/currency ratio.

3. Most of the remaining gold demand was in Europe. The Depression, rearmament, and WWII put enormous pressure on their economies, leading to a dramatic reduction in European gold demand.

Even so, by the mid-1960s US policy was so expansionary that there were expectations that we’d eventually leave the gold standard. Finally in 1968 we closed the gold window to foreigners (other than governments) and the free market price rose above $35. The gold standard was finished, never to return.

Why the 34 year phase-out? People today cannot imagine how entrenched gold standard thinking was back in 1933. Contrary to widespread belief even Keynes was vehemently opposed to a pure fiat money regime—instead favoring an adjustable peg to gold. The post-WWI hyperinflations were fresh in peoples’ minds, and if you talked about the virtues of fiat money in 1933, any “Very Serious Person” would have simply pointed to Weimar Germany. End of discussion.

By 1968 the post-war Keynesian model was dominant, and money had been pushed into the background—not to reappear until the Great Inflation reminded people of its importance.

Next we’ll develop a model of fiat money. It will also feature a price level determined by the supply and demand for the medium of account (which is now cash), but there are several important wrinkles that lead to dramatically different policy implications.

PS. You might wonder why all the inflation didn’t occur between 1933 and 1945, instead of continuing during 1945-68. After all, the three factors I discussed above all occurred in the earlier period. The answer is that the Fed hoarded vast quantities of gold during 1933-45, which held down inflation. Then they gradually reduced their demand for gold after WWII, and hence prices kept rising during the 1945-68 period.

PPS. Doesn’t silver now cost about 300 pounds per pound? That’s some serious currency debasement.

PPPS. I hope Brad DeLong is right, as I’ve spent most of my adult life studying the Great Depression:

Second, you never know what parts of history may turn out to be useful and very important. Ten years ago I thought that my curiosity about and interest in the Great Depression was an antiquarian diversion from my day job of understanding the interaction of economic institutions, economic policies, and economic outcomes. The fact that we had gone through the Great Depression, had learned lessons from it, and had incorporated those lessons into our institutions and policy processes meant that there was little practical use to going over it once again. Boy, was I wrong. History may not repeat itself, but it certainly does rhyme””and nothing made an economist better-prepared and better-positioned to understand what happened to the world economy between 2007 and 2013 than a deep and comprehensive knowledge of the history of the Great Depression.

Tags:

19. March 2013 at 12:29

Love these back-to-basic posts.

You particularly won me with reminding folk that silver was historically a much more important monetary metal than gold. It is remarkable how much difficulty some folk have with that. I remember reading one paper which defined “gold standard” as convertible to silver or gold. So, China spent much of its history on “the gold standard”, when it was NEVER on the gold standard, their monetary metal was always silver. China was driven off the silver standard in the 1930s by FDR’s pandering to silver state Senators. (One of my basic objections to the gold/silver standard is it makes your monetary system susceptible to destabilisation by other countries.)

No gold coins were minted in commercially significant quantities in Western Europe from the end of the Western Roman Empire to the 1200s. In fact, their re-appearance in the C13th is a sign that trade was recovering about to the level it was under the height of the Roman Empire (other signs include levels of shipwrecks in the Mediterranean and cook books). There was a historical fashion for a time to claim that the collapse of the Western Roman Empire was not a “fall”, it was a “transition”. Nonsense, trade collapsed in Western Europe and took the best part of a millennia to recover to its C1st/C2nd Roman peak.

Mind you, the Western European Dark Ages of the C5th=C11th century was mild compared to the collapse in the Eastern Mediterranean at the end of the Bronze Age around 1200BC. Literacy completely disappeared from Greece and much of Anatolia remained at village level for about a thousand years.

19. March 2013 at 14:33

I am going to have to think on this a bit more…. there is a lot here…

Declining demand for gold is expansionary. We left the gold standard in 1968 because us policy was so expansionary. When we left the gold standard the price of gold increased severl fold…Something about this is not logically following for me. What I am I not getting.

What changed in the dynamics for gold in the mid 2000s that after 2 decades at a price near 400, the price of gold began grow so quickly?

How would you describe the system of money from the middle ages through the enlightenment, when countries minted gold and silver coins, and a shilling was a shilling if it had the kings face on it. But, the sovereign could litterally debase the metalic content of the coins? It wouldn’t be quite right to call it a gold standard (or a silver standard).

19. March 2013 at 16:08

I’m liking these series of posts. Looking forward to the next ones.

———–

More minor quibbles:

I don’t accept the claim that “lower bounds” represent an economic problem that requires non-market intervention to “solve”.

It is real profit rates and real interest rates, combined with respect for property rights and economic freedom, that incentivizes investment, not nominal rates. Even if nominal rates are just 0.1%, there is nevertheless a huge incentive to invest if productivity is huge. If 0.1% profit represented a real gain that is clumsily regarded as a single rate, a real rate, say 20%, then it would represent a more attractive investment as compared to a different world where nominal rates are 20% and the (clumsy) associated real rate of return is 0.1%.

Even if a lower nominal rate of profit lead some people to hold more cash, then the long run result, which would occur more quickly than typically given credit for, would be for costs and prices to fall, but with an end result of higher nominal profits than otherwise, since the consumption out of dividend and interest payments that come out of cash balances, would bring about a higher rate of profit (since investment is lower, and thus costs are lower).

There really is no rhyme or reason to fear low rates of profit that are founded upon either high savings rates, or occasional changes in cash preference.

I agree with market monetarists that “lower bounds” (which are not exactly able to be zero for any appreciable length of time, since people have to consume SOMETHING) are not end of the world events. I just disagree with why they are not so. Market monetarists don’t fear them because they think that central banks can inflate regardless. I don’t fear them because I think the market process can, eventually, accommodate changes in cash preference that would make any resulting unemployment a fleeting phenomena.

I guess it would be timely to remark on Japan, since it is almost certainly in the mind of the reader. Japan’s sluggish real growth for the last 20 years is not due to insufficient money creation for the last 20 years. If inflation is low, then one would expect that after 20 years, people would have become accustomed to it by now such that their pricing behaviors would enable a tendency towards full utilization of resources and labor. It would be foolish to believe that people would work at and manage companies for 20 years, producing less because the change in prices from year to year is 1% instead of 2% or 3%. If people can become accustomed to 3% after 20 years, then they can become accustomed to 1% after 20 years.

The reason for the sluggish growth in Japan is a combination of factors besides low inflation.

One important factor is that most growth measurements are biased upwards in inflationary countries. It’s hard to track real growth, and real growth is measured as higher in more inflationary economies. It’s easy to see growth in spending, it’s harder to discern innovation, technology, and so on, from spending and prices.

Another important factor is that most growth measurements are looking at flawed and misleading indicators/data. GDP growth per year for example is highly misleading for a number of reasons.

A third important factor is that Japan’s demographics are shifting towards more welfare and less productivity.

A fourth factor is that Japan’s high debt level makes it unattractive for foreign investment. Imagine equity investors considering investing in 10 alternatives, where one has significantly higher outstanding debt. Debt overhang theory has a fairly large literature, and in general it states that when an institution has a high debt load, equity investors know that most of the gains that arise from their investment accrue to debt holders rather than equity holders. That brings down the attractiveness to equity investors. Lower investment, lower production.

A fifth factor is that Japan’s free riding in the world market is lower precisely because it is less inflationary. More inflationary economies have the seemingly paradoxical ability to increase their consumption by way of exporting currency, and importing goods. The US for example has done this with China for decades. Many of us, without much realizing it, are benefiting in part by the fact that we export dollars, and China imports to us real goods. That increases our standard of living beyond that brought about by pure productivity alone. Japan, because it isn’t inflating as much, doesn’t have the same luxury.

Notice that this last point, while seeming to agree with the argument that Japan’s tight money is decreasing their standard of living, is not quite the same thing as saying more inflation will increase their productivity. Their standard of living is lower because they are mooching off Chinese producers less than we are through exploiting China’s specific form of central bank intervention.

19. March 2013 at 16:37

Memo: money is not a commodity, it has always been debt/credit. Even when silver was used, it was as a medium to stamp a value higher than intrinsic, just like watermarked paper today. Amount of silver in vaults had no bearing on the value of money. Money is created out of thin air by banks and governments, there is no fixed pool of it, so plotting “quantity of silver vs its value” tells you nothing about the value of money.

19. March 2013 at 17:08

Thanks Lorenzo.

Doug, Once we left the gold standard the gold market became irrelevant. Gold prices rose as other prices rose during the Great Inflation–indeed faster because people hoarded gold. Of course gold hoarding is deflationary under a gold stnadard.

Geoff, You said;

“I don’t accept the claim that “lower bounds” represent an economic problem that requires non-market intervention to “solve”.”

I agree.

OhMy, You aren’t paying attention. I’m defining money as the medium of account. That was gold under the gold standard. So your comments are beside the point.

19. March 2013 at 17:51

Dr. Sumner:

“Geoff, You said;

“I don’t accept the claim that “lower bounds” represent an economic problem that requires non-market intervention to “solve”.”

I agree.”

I think you are agreeing with what could be interpreted as being consistent with the implications of that statement.

After all, central banking is non-market intervention. This second statement is one I had in mind. Wanting the central bank to create more monetary inflation, in order to bring about the observance of a statistical rule, could be interpreted as being consistent with the implications of this second statement, namely, that a specific form of non-market intervention is being called for when there is the lower bound: Inflate more dollars via “unconventional” OMOs.

19. March 2013 at 18:30

Money can be

1) backed by gold

2) convertible into gold

3) denominated in gold.

and/or several combinations thereof. There is also a broad spectrum of types of convertibility: gold convertibility, bond convertibility, CPI basket convertibility, etc. The whole idea of fiat money developed when people mistakenly thought that ‘inconvertible’=’unbacked’.

So before we develop the theory of fiat money, we should make sure that our currency is not, in fact, backed. The fact that all banks, central and otherwise, hold assets against the money they issue, indicates that fiat money is no more real than the phlogiston, ether, and caloric of early physical sciences.

19. March 2013 at 19:15

Via Russ Roberts twitter feed:

“I am finally figuring out Scott Sumner’s view of money. Coming Monday on EconTalk”

19. March 2013 at 19:34

The price level is determined by changing rates of productivity growth & changing production lengths & the changing reach of the domain of what is an economic good and what Is not.

QED

19. March 2013 at 19:38

The demand for silver as money varies depending on the suppy of and demand for substitutes for silver, eg depending on the supply, demand and liquidity of highly liquid near money asset substitutes for silver money.

QED

19. March 2013 at 20:35

Side note to Scott Sumner: Stephen Williamson has a recent post on “The Balance Sheet and the Fed’s Future.” Mar 10.

I read, re-read, re-re-read it and read some more until I got a headache.

Williamson seems to say we are in a liquidity trap, and so QE is powerless. The Fed could lower IOR, but since we are only at 0.25 anyway that is big whoop.

The answer is federal spending and issuing debt, says Williamson.

Sorry if you addressed this before.

I can’t imagine QE not working, if applied heavily and continuously.

Can you explain what Williamson means?

19. March 2013 at 21:00

Thank you for these more basic monetary posts. I find them very helpful and appreciate it! Please, please, continue, as your explanations are both thorough and comprehensible!

19. March 2013 at 23:58

Benjamin, I thought Williamson’s schtick was that it was structural and theres nothing we can do?

20. March 2013 at 03:20

[…] See full story on themoneyillusion.com […]

20. March 2013 at 04:18

Charger Carl-

In the post I reference, Williamson seems to be saying only federal deficit spending can help. That the federal government has to issue a lot of debt. A sort of combo monetary policy-Keynesian approach.

In his latest post I ask Williamson several questions. I ask if we printed up fresh cash and furtively left it in grocery bags in moderate-income neighborhoods at night, $100 billion a year, would that help. Or if we got overseas drug lords to come to the USA and start spending their Benjamin Franklins.

Williamson is clear that he thinks QE is worthless. I believe QE is like leaving bags of money on the street, but less effective. Some of the money will leak back into swollen bank reserves.

I am not a real economist, btw. But I sure would like to know what works, an even more important approach.

20. March 2013 at 04:43

Mike, In this example money IS gold.

Ben, I can’t take seriously the notion that we are in a liquidity “trap” I’ve blogged it to death, and the evidence is so overwhelming strong that we aren’t that it hardly even seems worth discussing. Do people not follow the Japanese stock and forex markets?

20. March 2013 at 04:58

@ssumner: Can we please NOT hijack this comment thread to discuss about something else? This is a very interesting post which non-economists like me can read, understand and follow the discussion along. Please request Benjamin Cole to bring it up elsewhere.

20. March 2013 at 05:04

“There is no quantity theory of money yet; that will come later with fiat money (although ironically the theory was invented during a commodity money period where it doesn’t quite apply.)”

What do you mean there is no quantity theory??

It clearly looks like the quantity theory to me! It does apply to increasing commodity money supply too. And also to money substitutes partially backed by commodity that existed at the same time. Not only to fiat money.

“You might wonder why all the inflation didn’t occur between 1933 and 1945, instead of continuing during 1945-68.”

You forget to mention all the price controls put in place by the FDR administration in the 30s. Prices soared once they were lifted.

20. March 2013 at 07:58

Dr. Sumner,

Great post. Much appreciated.

20. March 2013 at 08:23

Scott: This is also actually pretty interesting. So you claim that during the gold (silver) standard, gold (silver) was medium of account. By your definition therefore gold was money

Now I am really curious, because this would mean that if for instance velocity of circulation of paper currency under gold standard changes permanently – then this means (under assumption that Central Bank will offset this by selling/buying their gold reserves for currency) just a change in supply/demand for gold. The two things (change in velocity of paper currency and change in demand for gold) are not only equivalent, they are the same thing.

If one follows this logic, then if central bank pegs the currency to CPI basket then CPI basket and not dollar (Euro, Pound …) is money. So we can safely stop talking about people hoarding/disgorging cash, it is for all purposes of monetary economics exactly the same thing as change in supply/demand of items in CPI basket in the economy. It has to be, money is MoA by definition – remember? Now this is an excellent news, as it is one less thing to worry about. And as a side effect it enables macroeconomists to build models of economy without “money”.

20. March 2013 at 09:06

I understand easily enough the basic assertion that as the value of gold or silver (or the unit of account) rises, the price level falls.

What is the mechanism by which this price deflation occurs in a macro sense? I’ve never been able to walk my way through this “process” and have been waiting for a good opportunity to ask and hope Scott or any of the other economists here can explain it or recommend a website or paper that explains it consisely.

I apologize in advance if this is a foolish question.

Thanks

20. March 2013 at 09:35

Scoot

Your “opposite” exists!

http://thefaintofheart.wordpress.com/2013/03/20/a-scott-for-all-seasons/

20. March 2013 at 11:04

Saying that FDR took away American’s right to “hoard” gold is just about the most pro-state biased way of putting that possible. FDR took away American’s right to hold gold; confiscating it from private citizens and putting it in Fort Knox (created for just that purpose). By confiscating private gold and suspending redemption at $20.67/oz., the government was violating its expressed pledge and contract to the American people in order to rob them of purchasing power. Theft pure and simple.

20. March 2013 at 19:01

JN, The price controls of the 1930s forced prices HIGHER.

I meant that changes in the supply of the MOA don’t cause proportional increases in the price level. The QTM may still work for money as the MOE.

Thanks Randomize.

JV, If you successfully pegged the price level, then the value of money would never change. Nominal and real variables would always be identical.

However I think the purchasing power of dollars as a share of NGDP is the best definition of the value of money, hence it wouldn’t be the end of monetary theory for me.

Brian, I will address this in later posts, but it’s basically the “hot potato effect.” Since the price of gold can’t change, it’s value can only changes by other goods prices rising or falling to equilibrate the gold market. Expectations play a big role, as do asset prices.

Marcus, Thanks, I’ll take a look.

John, Economists don’t attach any normative implications to “hoard.” It simply means to increase one’s demand for money, or the MOA.

21. March 2013 at 14:01

Scott,

Yes increasing demand for cash is the positive term but hoarding seems to be used in a very normative way by many economists.

23. March 2013 at 07:23

John, They shouldn’t use it that way.

25. March 2013 at 17:56

Hi Scott,

Listened to you on econtalk today. For a laymen like me you really made my head hurt. Was curious why you think Gold is so high now if we are in such a deflationary environment and if you thought the actions of the Fed or peoples current expectations of their future actions will affect the price going forward? Do you think there is a sentiment in Asia that gold is money and that is why it is being bought by individual and central banks?

Thank you for your work,

Russ

1. April 2013 at 20:15

“Do people not follow the Japanese stock and forex markets?”

Got a kick out of that. 🙂

24. February 2014 at 09:50

The Socialist Myth of the Greedy Banker & the Gold Standard

http://iakal.wordpress.com/2014/02/24/the-socialist-myth-of-the-greedy-banker-the-gold-standard/