Krugman on monetary and fiscal stimulus

Recently I’ve wanted to comment on almost everything Paul Krugman posts. Here is a recent post where he discusses nominal GDP targeting:

But it would be a big mistake to count on monetary policy alone. The zero lower bound on short rates really does matter, even if longer-term rates are positive. The Fed can control short-term interest rates, it can influence long rates “” there’s a world of difference between those two statements. So it’s not safe to assume that the Fed can, for example, hit any target for nominal GDP that it chooses.

I think Krugman is confusing two issues here:

1. Can the Fed control actual NGDP perfectly?

2. Can the Fed create any desired expected rate of NGDP growth?

The answer to the first question is obviously no, due to policy lags. On the other hand there are no policy lags between changes in monetary policy and changes in expected NGDP growth. So in the reductio ad absurdum case where the Fed is willing to buy up all the world’s assets, and incur all sorts of price risk, then I think the answer is pretty clearly yes. And I would add that the answer is yes whether we are talking about internal Fed forecasts, or forecasts from an artificially created and subsidized NGDP futures market, or some sort of hybrid, such as having the Fed use TIPS spreads and estimates of the slope of the SRAS to generate the implied NGDP growth forecasts embedded in the market’s current inflation forecast.

The real question is whether such a policy would be so risky that it would not be politically feasible. I say no. If the Fed stops paying interest on reserves, and targets NGDP growth at a much higher rate than currently expected, then the real demand for base money would almost certainly be lower than today, not higher. When you target expectations, the monetary base becomes endogenous. So the question is not “How much money do we have to create to raise NGDP growth expectations up to the desired level?” Rather the question is: “What is the real demand for base money if the Fed does target a much higher NGDP growth rate?”

Krugman is too pessimistic on two different levels. In other posts he sees the currently bloated monetary base doing little to boost AD, and assumes that a much larger monetary base would be required to generate the appropriate level of nominal spending. He is an expert on the importance of central bank credibility, but doubts whether the market would find a more aggressive NGDP target to be credible. But if we target the forecast, then that’s not a problem. The Fed needs to do whatever it takes to make the policy credible. There may be some indeterminacy problems here, but they can be circumvented if you let the market forecast the instrument setting that will hit the target. And level targeting can greatly reduce any indeterminacy.

Krugman is also too pessimistic about long term interest rates. He wonders whether the Fed can reduce long term rates enough to get the desired nominal growth. But that is the wrong question to ask. The real question is “What is the equilibrium long term interest rate if NGDP is expected to grow at the target rate?” It is very likely that much more rapid expected NGDP growth would be associated with higher nominal long term rates, and there are plausible forward-looking models where even the real long term rate would rise with monetary stimulus (due to higher expected real growth resulting from reflation.)

Krugman might argue that all of my ideas are pie in the sky, and that the Fed won’t be willing to take these sorts of radical steps. And of course he’d be right. The longest journey begins with a single step. I am just trying to get people to think about these issues from a Svenssonian perspective—TARGET THE FORECAST!

Part 2: Did Keynesian stimulus work in Asia?

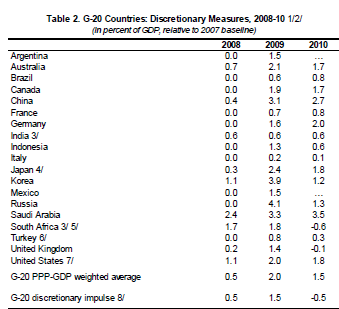

Maybe, but how would we know? Krugman says we know from this table:

In early 2009, the IMF estimated the size of stimulus programs (pdf) in G20 countries:

.

I suppose Korea would present the best case for stimulus. But Krugman himself has warned us that you can’t look at fiscal policy in isolation, you also need to consider what was happening to exchange rates. The Korean won fell from somewhere in the 900s (to the dollar) in early 2008 to somewhere in the 1400s in late 2008. That’s a pretty massive devaluation for a trading nation. In 2009 the won partially recovered, as the Korean economy rebounded, but remained far below early 2008 levels. In contrast, the Japanese yen has actually appreciated against the US dollar during the current recession. And remember that Japan and Korea are close competitors, both selling products like cars, ships and electronics. Is it any wonder the Korean economy has done better than the Japanese economy? Indeed given the dramatically different paths of their exchange rates, I’m surprised the gap in economic performance isn’t even bigger. Of course the same argument applies to China, which stopped appreciating its currency once the crisis hit. Given the rapid productivity growth in China (and the Balassa-Samuelson effect) a stable yuan/$ exchange rate is equivalent to depreciation of the yuan.

.

It’s also worth mentioning that the sort of stimulus done by China could not possibly have been done in the US, even if we had wanted to. The Chinese go out and build subways, high speed rail and airports at the drop of the hat. We’d probably need at least 5 years to get the necessary permits and fight off all the NIMBY lawsuits, maybe 10 years. We could do tax cuts quickly, and I favored cutting the employer share of the payroll tax in order to overcome wage rigidity, but Krugman argues that those are the sorts of fiscal stimulus that are the least effective. So there was no prospect of the US following the lead of China, and there is very little evidence that differences in the size of fiscal stimulus packages explain differences in economic performance, particularly when other variables such as exchange rates are brought into the picture.

.

BTW, I think the Chinese stimulus did probably boost GDP. But how much was actual government spending, and how much was regulatory changes making it easier for state-owned banks to make loans to state-owned firms? They have a very different system.

.

PS. David Beckworth also comments on Krugman.

Tags:

25. July 2010 at 14:17

Scott, please stop acting like we do not have an immediate way to spur massive private investment, even at higher interest rates. I’ve given you two: liquidate foreclosures and privatize government services. Both of these will get the cash out of the mattress.

Sure, stop paying interest on reserves, but then foreclose on every 90+ day late home backed by Fannie and Freddie. Auction them all immediately only to private investors with 30% down. We’ll have 1M+ homes sold cheap – start everything at $1 auctions.

The economic activity will be just as meaningful as building a railroad in China. Bring back mark-to-market, and liquidate the truly insolvent banks. People with cash LOVE DEALS. Banks that aren’t insolvent will happily finance a super cheap home loans with 30% down.

Think of it as QE, but by moving the non-performing assets to the balance sheets of private individuals and not zombie banks.

The debts have already been defaulted on. The government has already securitized these loans. Who cares what happens to home prices? Not you! Why are you so determined to keep these zombie banks from facing the music?

25. July 2010 at 15:48

I’ve lately been *very* disappointed in the way Krugman presents data on his blog. You can almost always tell whether the data actually tells the story he says it does by the way in which he presents it.

What’s with a hard-to-read table of merely discretionary measures without a column for some metric of “improvement”?

The “Asia Keynes” story, for example, just *begs* for a scatter plot. Something like “total deficit-financed expenditures beyond pre-crisis government baseline (‘fiscal stimulus’) vs. gap between current conditions and extrapolated pre-crisis trend of growth”. Boy, wouldn’t that graph, if it showed a nice straight line, make the greatest case in the world for Keynesian fiscal stimulus – somebody should make it!

One would think that it would take a team of wild horses to restrain a Nobel-prize winning international trade economist and public intellectual from making and publishing such a persuasive chart. On the other hand – it the scatter was mostly a cloud, it would tend to make the opposite case, or need all sorts of explanations and corrections and hand-waving. I wonder what the graph looks like… without making it, I think I can guess.

Krugman also occasionally takes, um, “questionable liberties” when both 1. Choosing start and end dates of a chart, and 2. Sketching “trend lines” based on charted data.

You know, for such an expert on credibility …

25. July 2010 at 18:00

http://www.youtube.com/watch?v=f8JGhVPO90g

25. July 2010 at 18:33

Professor Sumner,

In both Bernanke’s recommendations to Japan in the 90s and now, lowering the exchange rate of the currency is a way for the central bank to stimulate.

How is this stimulating? Is it simply more stimulus the same way FOMC always does by putting more reserves in the market, or is it simply nothing more than helping exports to increase?

If its the latter, why not prefer a higher currency, since this would bring in more investment? Why is exchange rate devaluation preferred?

25. July 2010 at 19:35

Another deeply insightful blog by Sumner.

Frankly, I think the world (well, US policymaking community) will come to Sumner in the next six months. We will see deflation and stagnation, and more deficit spending is not in the cards.

No one wants high inflation per se. But I would rather live through an long inflationary boom, and than a long deflationary recession.

Time will tell–but as scared as Bernanke is of inflation, he is more scared of deflation.

25. July 2010 at 23:08

Do you see any pattern? I sure don’t

Yes, that does seem to be about right: with a reasonable data set of countries, there is not much correlation between fiscal stimulus and gdp growth.

26. July 2010 at 03:32

Yesterday I left a comment on Krugman´s blog. In it I wondered why, if in the 90, for Japan, he was an ardent advocate of monetary policy, today he has changed to the field of fiscal policy pure and simple, and has become an “old Keynesian.”

My comment has vanished … why? so terrible is it?

26. July 2010 at 05:53

Got a surprise for you: Yglesias is singing the same tune.

”

Timothy Geithner has already received appropriations to buy printer paper and toner cartridges for the Treasury Department. If Ben Bernanke is inclined to play along, there’s no bar stopping Geithner for literally firing up his word processor program and printing out pieces of paper that say “Take this to Ben Bernanke and he’ll give you $10,000.” Call such pieces of paper Geithnerbucks. Geithner can’t turn these Geithnerbucks into legal tender, but the Federal Reserve bank can decide to “buy very unconventional assets” such as pieces of paper printed out by Timothy Geithner. Such action, if undertaken at any substantial scale, would almost certainly cause people and businesses to become less inclined to hold cash and more inclined to trade their cash for some goods and/or services.

“… What’s more important is how the Fed frames what it’s doing. If the Fed says it’s determined to push the price level up, and will keep trying things until it gets up to such-and-such a point then that will probably work. Conversely, if the Fed says it’s willing to intervene to prevent a total economic collapse but beyond that is determined to pursue a strategy of opportunistic disinflation then we won’t get robust recovery.”

26. July 2010 at 06:45

[…] week at best. In the meantime, here is Krugman’s thinly-veiled critique of Scott Sumner, and here is Scott’s […]

26. July 2010 at 08:46

Should NGDP grow at 5% if it requires creating artificial incentives for wasteful economic activities? That is, if hitting that target would require people to hastily commit resources to projects of dubious merit?

26. July 2010 at 09:31

Prof. Sumner, you said:

“It’s also worth mentioning that the sort of stimulus done by China could not possibly have been done in the US, even if we had wanted to. The Chinese go out and build subways, high speed rail and airports at the drop of the hat. We’d probably need at least 5 years to get the necessary permits and fight off all the NIMBY lawsuits, maybe 10 years.”

I thought the effect of the stimulus occurs instantly once the bill is signed? Or are you saying that it would have taken that long to even get a stimulus bill like China’s finished and signed into law? Or am I missing something completely?

26. July 2010 at 10:19

Morgan, See my new post on housing.

Indy, I agree. Lorenzo (below) provides just such a graph. It’s not a very impressive correlation.

Joe, I see currency depreciation is a symptom of easy money. Even if you don’t explicitly try to devalue, a policy of very easy money will often depreciate a currency. I don’t see it working primarily through exports–the US trade balance actual got worse after the 1933 devaluation, as rapid growth sucked in more imports.

Thanks Benjamin.

Lorenzo, Thanks. Yes, I saw that graph as well. Not impressive.

Luis, Sounds like DeLong’s blog.

D. Watson. I like Yglesias’ blog, despite our political differences on some issues. His views are definitely close to mine on the Fed, and he cites me sometimes. I suppose he has always favored easier money in a recession, but I think some of my posts may have influenced the specific arguments he uses. If so, that would be great.

Silas, It never forces people to do anything (which I agree would be unwise) They can keep producing the same real output, and then we get 5% inflation. I don’t see it as a policy change, I see the sudden drop below 5% NGDP growth as the policy change. I want to get back to a neutral policy stance.

Tim, Good question. One response I could give is that we will probably be out of a liquidity trap in 5 or 10 years, and even Krugman admits that the case for fiscal stimulus hinges on rates being stuck at zero. You are right that if the fiscal stimulus caused the expected price level 5 or 10 years out to rise, that would raise inflation expectations and AD right now. But the Fed would presumably not allow inflation to rise once we are out of the liquidity trap.

But it is still a good argument, and I forgot to take that into account. Oddly, I was thinking more along the lines of the way my intellectual opponents think about the issue.

26. July 2010 at 11:21

“The real question is whether such a policy would be so risky that it would not be politically feasible. I say no. ”

Perhaps the forecast we target should be 5% NGDP growth with a bias towards less intervention if our inflation volatility forecast is too high.

You could package an NGDP future with an inflation call struck at 10% or something. Normally that’ll be near worthless and so have very little effect compared to your current plan. But, at some point if too much QE is “too risky” then the value of the package will be such that market participants will stop selling before generating sufficient OMO to get to 5% expected growth. If we care about riskiness, then this could be optimal.

26. July 2010 at 11:35

@Scott_Sumner: To make people continue to believe there will be 5% NGDP growth, the Fed has to make loans to *someone*. What ensures that these loans will be where they’re needed, rather than propping up part of the economy that needs to liquidate?

26. July 2010 at 13:46

Thanks for the answer Professor Sumner. I had a feeling you may have been “getting into the heads of your opponents” when you wrote that.

27. July 2010 at 05:59

fmb, Interesting idea, I’d have to think about that a bit. But it might be worth pursuing if you are worried about volatility. I think with level targeting there would be less volatility thatn people believe.

I’d do that with NGDP growth, by the way, as 10% inflation is not a problem if NGDP is on target.

Silas, The Fed should simply buy Treasury bonds.

Tim. Yes, I supposed my mind gets distorted by reading old Keynesians.

27. July 2010 at 07:05

@Scott_Sumner: That’s even worse! How do you know that the government projects thereby facilitated aren’t wasteful?

27. July 2010 at 08:22

To be clear: I tend to agree that there would be less volatility. But, it seems that the most common response of people who generally seem to get the idea (e.g. BB, PK) has something to do with risk. The right response seems to be not “don’t worry, it’ll be fine”, but rather “well, how do we get a market forecast of that risk?”

28. July 2010 at 08:16

Silas, That doesn’t facilitate government projects–the Treasury would sell the bonds to the Chinese or Germans if the Fed didn’t buy them.

fmb, I’m not arguing against you, but I can only do so much at once. Just talking about targeting NGDP futures contracts is really strange to most people. Adding in options further dilutes the message. Once the topic becomes discussed more widely, then we bring in thes extra wrinkles.

Krugman’s fear is price risk to Fed assets, but that’s not a problem under my plan, as I would have them buy low risk T-bills and T-notes.