Do demographics explain disinflation?

No they don’t; monetary policy determines the rate of inflation. But the Wall Street Journal’s “Daily Shot” sees things differently:

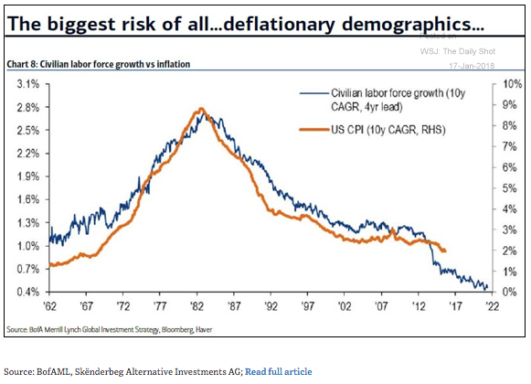

Over the long run, economists think that demographics dictate inflation trends. The collapsing US labor force growth is expected to be a drag on the CPI.

Really? I’ve never met an economist who thinks demographics determine inflation. Now let’s look at the graph the WSJ uses to back up this claim:

People are far too impressed by this sort of simple correlation. Let’s look at what the statistician had to do in order to make labor force growth and inflation look correlated:

People are far too impressed by this sort of simple correlation. Let’s look at what the statistician had to do in order to make labor force growth and inflation look correlated:

1. The scales for the two lines are completely different. The left scale shows labor force growth, and tops out at 2.8%. The right scale shows inflation, and tops out at nearly 9%.

2. Both graphs use 10 year moving averages, which smooths out a lot of the short term volatility.

3. The civilian labor force graph uses a 4 year lead, to make the peak growth rate line up with the peak inflation rate.

If the data were any further massaged it would turn into a bloody pulp.

Here’s what people often do. They find two time series that each have a long period of upswing, followed by a long period of downswing. They could have just as well have used interest rates, or some other variable. But they chose inflation and labor force growth. Then they smooth the data, adjust the two scales so that each peak has the same height, then use leads or lags to make the peaks line up on the horizontal axis as well.

Even worse, they use two series that are not linked according to any economic theory that I am aware of.

This is too sloppy to get published in an academic journal. But the stuff that does get published is often flawed in a similar way, just to a much lesser extent. The errors are more subtle.

PS. Check out US labor force growth rate from 1865-96 (high). Then check out the rate of inflation (negative).

HT: Daniel Griswold

Tags:

18. January 2018 at 19:36

Putting on my monetarist hat for a moment, I think this claim is even worse than it seems: if we assume constant per capita GDP at y, for instance, and write the usual MV = PY in the form MV = PNy where N is population, then with constant velocity we get m – pi = n where lowercase letters denote growth rates, so if the monetary authority just has a fixed money growth rate policy, lower population growth should mean higher inflation (because there’s less aggregate real money demand). Money in the utility function models give a similar result.

I think this is just part of the broad tendency to confuse nominal things with real things; lower population growth (or population decline) means “less demand”, and “less demand” should mean “lower prices”. If people could distinguish between “real demand” and “nominal demand”, and understood that the monetary authority steers the nominal economy, we wouldn’t see articles like these.

18. January 2018 at 20:52

It is not uncommon to encounter this type of argument / illustration from “experienced” portfolio managers managing multi-billion dollar bond funds and fixed income mandates. It drives me nuts, but I guess it is just difficult to explain how “demographic dividends” actually work: i.e. fall in birthrate triggered by better development policy.

But then I sometimes send in-house fixed income managers this link whenever they make this mistake.

http://www.tylervigen.com/spurious-correlations

My favorite is # of people who drowned by falling into a pool vs. Films Nicolas Cage appeared in…

18. January 2018 at 21:02

Professor Sumner,

Might it be fair to say that demography indirectly affects inflation via affecting r*? Your counter, I would presume, is that monetary policy, especially under an NGDP-targeting regime, is nonetheless able to control the inflation rate and, and for a fixed growth rate embedded in the level rate, a lower r* that spells lower trend RGDP would lead to higher long-run nominal rates (and, to the extent demography were an issue, real interest rates should fall by enough to generate a sufficiently negative real interest rate gap). But we could counter — playing Devil’s Advocate here — that demography may be hard to measure in real time or even to forecast, and thus there could be systematic misses.

Personally, I’ve been very hesitant to accept the old dictum “inflation is always and everywhere a monetary phenomenon.” This absolutely should be true, but having experienced the last few years of plummeting commodity prices and the era of ‘transitory’ influences holding down inflation (even price competitiveness in the form of Amazon is now being blamed for this), I feel a better revision might be ‘nominal stability is always and everywhere a monetary phenomenon; inflation over the LONG RUN is strictly a monetary phenomenon.’ This meshes quite well with your argument that NGDP is the best counter to a supply shock (or Jeffrey Frankel’s argument that it counters well a terms-of-trade shock). These arguments are even more important at a time when price-level targeting is getting so much attention (that should be going to NGDPLT, I honestly believe.)

This is all perhaps beside the point, though. Great catch on that WSJ article. It’s amazing what the editors allow their writers to get away with…. Hopefully they retract this piece.

18. January 2018 at 22:03

Ege, Good comment. I suppose slower population growth could slow V by lowering interest rates, but as you say it’s a moot point as the central bank controls inflation.

18. January 2018 at 22:24

Fred, Demography is fairly easy to measure in real time, and in any case these graphs look at 10 year averages.

In addition, real interest rates were quite low during the 1970s, when inflation was high.

I agree with much of your comment, however.

18. January 2018 at 23:13

Scott,

I’m not sure what the impact of lower population growth would be on real interest rates – our asset pricing models operate at the level of the individual investor, i.e the marginal utility growth in the discount factor depends on per capita consumption, not consumption. You can get away from this result by assuming parents value the utility their children will get from consumption as well and try to save for them, but then you have to take into account how exactly parents value the utility their children will get from consumption (because it influences saving and investment behavior and thus the level of consumption today) and how the number of children interacts with that, and we’re in territory where the conclusions we draw will not be robust to changing specifications.

Here’s a very simple model to illustrate: take an economy with per capita inelastically supplied labor and constant returns to scale and only labor input production technology. There are countably many periods, each person lives for one period, earns income from labor, has children (I assume pop growth is exogenous) and dies. Goods are perishable and there’s no aggregate investment. Take a standard utility function u and assume a parent maximizes \sum_{k=0}^{\infty} b^k N_k u(c_k) where N_k is the number of descendants they have at period k. Then, the asset pricing relation remains exactly the same as in the traditional case, and the real interest rate is independent of the process N_k. This result, of course, is unique to this specification and is not robust (there are two competing effects which cancel each other out exactly in this specification). I think it’s interesting to explore what happens if we allow for investment and such, but I’m sure someone has done that already, and a comment isn’t the appropriate place for something like that.

All of this is irrelevant to inflation behavior, of course, but I think this is an interesting subject to think about.

19. January 2018 at 03:25

Good post.

Here is a odd one: The Fed is targeting a 4.75% rate of unemployment, up from 4.1% today, and plan to get there by reducing monetary accommodation. The Fed believes 4.75% is the bare minimum rate of unemployment to avoid NAIRU. At that level, you have about 1.5 people actively seeking work for every job opening.

“With the gradual removal of monetary policy accommodation, we expect the unemployment rate to return gradually to our estimate of the natural rate of unemployment of 4¾%.”

https://www.frbsf.org/economic-research/publications/fedviews/2018/january/january-11-2018/

But! The GOP just passed corporate tax cuts.

So, we could see higher unemployment and record corporate profits?

Boy, that’s the way to sell free enterprise to the voting public.

19. January 2018 at 04:29

A possible mechanism low demographics → low inflation could be low demographics → low GDP growth → low investment (by accelerator) → low natural interest rate → low inflation if the interest rate becomes higher than the natural interest rate.

19. January 2018 at 04:41

I think at some point I had either written an email to you about demographics or NGDP, or maybe I had just written it up and never sent it…

Anyway, I think about this from a cointegration perspective. I.e., what kind of cointegrating relationship is there between employment, the labor force, and NGDP.

Instead of the plot of labor force growth and inflation growth, I would focus on the plot of log labor force vs. log NGDP. It turns out that the two are pretty strongly cointegrated. The plot looks great. It makes sense too as nominal labor income (employment times average nominal wage) is by far the largest part of NGDP and the relationship between employment and labor force is mean-reverting.

The conclusion I draw from my preferred plot is that we saw a huge increase in the labor force as the baby boomers finished high school/college and more women entered the work force. The Fed acted in such a way that generated faster NGDP growth. Why did they do this? I suspect because the large growth in the labor force should have put downward pressure on wages, but instead it led to a large increase in unemployment. The central bank tried to respond to the increasing unemployment by goosing inflation and putting downward pressure on real wages.

I would need to check how this plot holds up in the 1865-1896 period. That data isn’t as easy to come by. However, I have done some of my preferred plot with other countries (over the post-war period) and it looks similar. I think there were some exceptions, but I wouldn’t call it a universal theory.

19. January 2018 at 06:48

Scott –

The question of inflation rates — or more to the point, interest rates — and demographics is an important issue and poorly understood.

In an article I wrote for the National Interest, I look at Japan’s long term demographic outlook and its implication for GDP growth and government taxes, spending and debt.

On the third graph down, you can see interest rates, GDP growth rates, and changes in Japan’s workforce. It is plain to see that a decline in the workforce has been accompanied by both a decline in GDP growth and a decline in long term interest rates.

Importantly, Japan’s GDP will likely be no higher in 2050 than it is today, barring some productivity miracle. It’s workforce will be 1/3 smaller, with offsetting productivity growth holding GDP steady.

Thus, we have a stagnant economy in aggregate with demand for real estate falling year after year. If you buy an apartment today in Tokyo, there’s a pretty good chance it will be worth less every subsequent year.

Now, what interest rate pairs with this development? Is it possible to have, say, 6% mortgage rates when real estate prices are in secular decline? I do not doubt that the BoJ could cause inflation if it so desired, but it seems to me that a shrinking workforce will likely be accompanied by low interest rates.

This in turn has implications for fiscal policy. Under earlier circumstances, interest expense put a limit on government borrowing. However, if interest expense is effectively zero, then borrowing is limited only in quantity terms, and for a country like Japan — or the US — could easily exceed 200% of GDP.

And in fact, that’s what we see in the US, as the Republicans have doubled down on the Democrats’ deficit, with social problems now solved not by GDP growth, but by ever increasing borrowing.

Therefore, to close the loop, I would be interested in your view on what interest rates might pair with a declining workforce, and the resulting implications for fiscal policy.

‘Japan’s Lost Century’, on my website here, with a link to the Natl Interest version: http://www.prienga.com/blog/2017/7/20/japans-lost-century

19. January 2018 at 07:23

A couple of more thoughts for Ege.

First, do people actually desire more children? It is not clear to me that they do in the modern world.

Second, what is Malthusian subsistence? In the popular imagination, this is starvation level. But in most natural ecologies, animals do not starve (due to predators).

If we use a more mathematical definition, subsistence could be defined as a population unable to maintain its numbers. By this standard, Japan and Western Europe are already Malthusian economies–but at quite high levels of income. Thus, we need to be careful not to confuse the concept of Malthusian subsistence with poverty or starvation.

As for the central bank controlling inflation, this control might be quite constrained. At 200% debt-to-GDP and no GDP growth on the horizon, a 1% increase in interest rates implies, in Japan, about a 6% increase in tax rates or a 6% decrease in spending as debt is fully refinanced (which could take some time). Any needed adjustment would run straight through the fiscal equation, because the economy cannot grow its way out of its debt load.

Thus, the central bank cannot raise inflation without precipitating a fiscal and related societal crisis. It has become a banana republic, but in exactly the opposite sense of, say, Argentina. Whereas Argentina is tempted to use inflation to solve spending needs, in Japan, a declining population, the absence of GDP growth and a high debt-to-GDP ratio discourages the central bank from turning to inflationary measures to prop up the economy.

19. January 2018 at 08:38

Ege, If you add investment to the model then lower pop. growth will generally reduce interest rates.

Miguel. More likely it is a spurious correlation. Why would the Fed want to behave that way?

John, I assure you that it won’t hold up for the 1865-96 period. Just the opposite.

Steven, Not sure how your comment relates to this post. No one denies that lower labor force growth may lead to lower GDP growth and lower real interest rates. But this post is about inflation.

19. January 2018 at 09:30

scott, where could i find the data from 1800s. FRED seems to only go back to 1913 for CPI and 1948 for Civilian Labor Force.

19. January 2018 at 09:32

Steven,

You are confusing nominal and real interest rates. Raising nominal interest rates with an easy money policy does nothing to the long run cost of debt service for the government, it just creates inflation. In the short run, it will be equivalent to a partial default on long maturity debt, so it will improve the fiscal situation.

Europe and the US are not at Malthusian subsistence, because they have sustained output per capita growth. Malthusian subsistence is the constant output per capita steady state of endogenous population growth models. In the modern world, I don’t think the difference im attitudes toward having more children is cultural; I think it’s caused by higher log marginal returns on human capital investment. This is irrelevant to my model, since it has exogenous pop growth.

Scott,

I am not convinced – this result seems far too strong to me intuitively. I’m writing from my phone now; when I have time I will work this out in a model with investment and report back.

19. January 2018 at 11:59

I think the inflation situation is a bit more complex.

Imagine a country with GDP of 100, taxes of 35, spending of 37 and 200 of debt carried at zero percent interest. In this case, the deficit is 2 of 100, or 2%.

Now imagine we increase the inflation and nominal interest rate to 2%. GDP is now 102, taxes are 35.4, spending before interest is 37.4 and the deficit pre interest payments are 2. However, with nominal interest rates now at 2%, interest payments rise to 4, and the total deficit rises to 6.

This is all fine and good if you can refinance the 4% interest payment, ie, if you’re willing to raise borrowing from 2% of GDP to 6% of GDP.

If not, for example, during a financial crisis, then the budget hits the wall right up front, and you either have to reduce spending or increase borrowing by 5.5% for each 1% point of inflation that translates into nominal interest rates.

Do I think this likely makes a central bank cautious about raising inflation in a zero interest rate environment? Yes I do.

Inflation converts principal payments into interest payments and front loads debt service, in effect. I do not think policy-makers are indifferent to the outcome.

19. January 2018 at 12:02

What determines the level of the constant output per capita, Ege?

19. January 2018 at 12:24

Keenan, Not sure, but prices fell pretty steadily from 1865 to 1896, while labor force growth was quite fast. So clearly the model doesn’t fit at all.

Ege, Here’s the intuition. Imagine capital is homes that never depreciate. With zero population growth there is no home construction, with 1% population growth there is $X investment in home building. With 2% population growth there is $2X investment in housing. So a small increase in population growth (which would presumably have little impact on aggregate saving) will dramatically impact the demand for investment spending.

We see very low interest rates in countries like Japan, with falling population, and unusually high rates in places like Australia, with higher than normal population growth.

19. January 2018 at 12:55

I think that Carrying Capacity is not constant, but rather a function of other factors in human society.

In an animal society with no birth control, a strong desire for sex, and no competition to children, sure, I think carrying capacity is a valid idea. I use it myself.

However, the Malthusian idea that people will reproduce willy-nilly (so to speak) once birth control is introduced is a more tenuous concept, I think.

People plan their families nowadays. I think both societal expectations, cost and opportunity cost are big factors in decision-making.

Parents want their children to grow up with the same or better opportunities than they had. Thus, the cost of child rearing, especially education, is a major driver. It is the declining return on investment in human capital which is causing people to have fewer children, among other factors. For example, if the cost of schooling fell by half, then people would probably have more children, ceteris paribus. Right now, many parents really struggle with education costs, and this does not seem to be getting much better.

Next, children have become luxury goods. They compete with other luxury goods, like BMWs, vacations in Aruba, and weekends in the Hamptons. I would argue that the joy of children is largely unchanged, while the alternative uses of time to children have vastly increased. For example, one could be talking to one’s children or alternatively posting a comment on a blog, something not possible thirty years ago.

Finally, children are not necessary for old age support, and thus children as an investment, rather than as a high-priced luxury good, is no longer valid. However, this behavior is built on the assumption that someone else will have those children if you don’t. This is exactly the problem of Japan: no one is having those children, and therefore the pillars of the economy are disintegrating over time.

Put it all together, and the Carrying Capacity of society may well be declining over time even in the face of increasing per capita output, because capacity is determined by 1) the subjective expectations of parents for the future of their children and 2) increasing availability of alternative activities to raising children.

If so, then I would argue it brings us back to my definition of a Malthusian society as one which cannot reproduce itself. Japan as a society is not doing fine. It is in long term decline, which if not reversed, will ultimately lead to the extinction of the nation.

19. January 2018 at 13:40

Dr. Sumner and Ege,

Monetary policy only works so long as the central bank is willing to change its stance. It’s the banks’ unfortunate failure to do as much as they need to do that’s left people grasping for other explanations.

19. January 2018 at 14:45

Steven,

You’re just stating the usual result that inflation leads to nominal budget deficit figures being overstated. (Here is a post from Greg Mankiw on this exact subject: http://gregmankiw.blogspot.com/2006/05/budget-deficit-shrinks.html) The actual debt burden of the government is real, and the “real deficit” (the one that actually puts a burden on the government) is the change in the real debt stock, which is still changing only by 2 in your argument, since a change of 4 comes from %2 inflation on the nominal debt stock of 200. (This is all up to first order approximation.) Inflation has no effect on the government’s ability to service its debt in this sense. In fact, Milton Friedman famously argued that one reason the US government allowed a period of high inflation in the 1970s was because inflation artificially pushed people into higher tax brackets and raised overall tax revenue as a share of GDP, so it actually improved the fiscal situation even more than the default argument alone.

I don’t think carrying capacity is a good way to think about human populations. The result you are probably reading on my blog *assumes* that families engage in planning, it doesn’t assume that they act like animals. It’s just that the end result looks similar if you work under a specific choice of functions in the model. The model also doesn’t treat children as investment for the future. If you try to fit human population dynamics to a simple logistic growth law, you will end up saying things like what you are saying now. Think about incentives, think about why people have children, what costs are associated with having children, and what might’ve led to the “cultural” change in attitudes towards having more children.

Yes, if the cost of schooling fell by half, people would choose to have more children. To get the human capital results, you need to factor in effort and time management, not just the fixed income costs associated with having children. “Human capital investment” here is supposed to be understood as an investment of *time*, not an investment of physical resources. That’s how you get the results Lucas gets from his growth models.

I am not taking your bait on Japan.

Scott,

I think we need to be more precise here. I can fully understand how a sudden influx of immigrants into a country would raise house rents and prices temporarily, and would also raise rents on other kinds of capital and affect real interest rates that way. However, take the model I outlined in the above post and say that production per capita is a function of capital per capita, so f(k), and that there are aggregate savings. With no depreciation, we can find a steady state of the model in which dk = 0, and so dc = 0 as well; and the result is once again that the real interest rate in steady state is independent of the population growth rate.

What about the impulse response to a sudden jump in population growth? The dynamical system here in C-K space is locally saddle path stable, so what happens is that in response to a jump in population growth, we just get an immediate jump in consumption to its new steady state value with the capital stock unchanged. There’s more *saving*, because population growth acts as a form of depreciation on capital per capita, but *interest rates* remain identical. This is something we can reconcile with your housing example, because things play out exactly as you said in terms of investment, but there’s no effect on real interest rates in this specification.

19. January 2018 at 15:36

I’m pretty sure Belarus has had negative population growth and high inflation occurring simultaneously.

The “headwinds/structural forces” approach exonerates central banks from their failures. CB’s are especially ill trained to respond to supply shocks under the dogma of price level targeting, does it really make sense to contract aggregate demand in response to a supply shock? Which is worse, high unemployment/greater dis-coordination or a one off jump in the price level?

19. January 2018 at 18:49

I am not a monetary economist… but where is the formal econometrics. Let’s try to settle this empirically where I can at least add some value.

19. January 2018 at 20:27

Reading The National Review, I conclude that it is Don Trump holding inflation in check while delivering a rip-roaring economy.

In 365 days, Trump has brought American from doom to boom.

“The first anniversary of the Trump Era finds Americans great again.”

Read more at: http://www.nationalreview.com/article/455604/trumps-inauguration-anniversary-great-year-america

The Trump Legacy is yuge—and already. No need to burnish a hagiography later, ala Reagan.

20. January 2018 at 13:52

Ege, I don’t doubt that you can write down a model where population growth has no impact on interest rates, but you can also write down other models where it does have an impact. And those other models seem like a better fit for the empirical evidence.

Having said that, I’ll keep an open mind–I certainly don’t have any sort of strong proof for my claim.

Student, I very much question whether “formal econometrics” is all that useful in macroeconomics. Do you have evidence for that claim?

20. January 2018 at 13:59

Ben, That may be the single dumbest article I read all year. America is great again because Trump created 1.8 million jobs? Is that a joke?

20. January 2018 at 14:48

Scott,

I can get behind that (that’s what I meant when I said that the conclusions are not robust) – my point was that if population growth does have an effect on interest rates, that mechanism is not as obvious as people (even in one of the comments here, where a commenter claims low population growth leads to lower r*) make it sound like it is, which is why I am agnostic about the issue.

20. January 2018 at 19:46

Scott re The National Review:

Yes, the magazine of William F. Buckley has seemed to have hopped off the rails, even if one agrees with some aspects of Trump-o-nomics, such as corporate tax cuts.

Trump is an alienating figure, but to the establishment GOP he delivered the tax cuts, kept the US deeply embedded in the Mideast and expanded the national security state, and only blabbered about building a wall. Would Jeb! Bush done any different?

Yes, on trade, maybe Trump will wonder off the reservation on an issue or two. but remember Reagan and Nixon? Cato Institute called Reagan the most protectionist president since Hoover, and possibly eclipsing even Hoover. But Reagan (or his public persona) was and is loved.

So, some protectionism seems acceptable.

Trump is a vulgar vaudeville act, and Reagan was class act (they were both showmen at heart), but on implemented policies, how can anyone tell the difference?

21. January 2018 at 08:12

Benjamin Cole,

I thought you believed the labor market was pretty weak, is Trump really doing anything to “hold inflation in check” beyond the continuing marginally tight (~3-4% NGDPg) stance of monetary policy?

The real issue is that anything Trump has done isn’t durable if republicans lose control of congress and the presidency by 2020. So much depends on his ability to keep republicans in office and betting markets/polls do not look good on that front. Good appointment with Gorsuch though.

Even though I despise Trump, he could be good on certain issues if he didn’t happen to be as likable as Harvey Weinstein. I wouldn’t be surprised if President Warren undid every deregulation/tax cut by Trump yet kept his protectionist policies.

21. January 2018 at 18:37

Cameron:

I do believe the Fed’s peevish fixation on labor “shortages,” and its genuflection to the Philipps Curve and NAIRU totems is bad macroeconomic policy, and probably reflects a ample dollop of old-fashioned class bias.

The Fed, believe it or not, is actually targeting a higher unemployment rate—4.75%—than the US has now. How nice.

Too bad. Labor participation rates are climbing. Even productivity is again rising and unit labor costs are falling. This is an economy becoming healthier for everybody.

I was commenting facetiously when i said Trump held inflation in check while ramping up growth—I was quoting the National Review.

Trump’s corporate tax cuts may be positive, we will have to see.

Add on:

I wonder if shrinking populations are disinflationary or even deflationary to the extent that housing costs start to fall. Inflation, as measured, is some large fraction housing, 30% or so.

Selgin has pointed out a few times that, yes, inflation or deflation are monetary phenomenons, but things can happen. A corn bust can raise prices as measured, even if monetary policy is tightened.

I would guess accumulating and chronic housing surpluses would lower inflation, as measured.

22. January 2018 at 07:56

“[M[y point was that if population growth does have an effect on interest rates, that mechanism is not as obvious as people (even in one of the comments here, where a commenter claims low population growth leads to lower r*) make it sound like it is, which is why I am agnostic about the issue.”

In terms of theoretical economics, this view might be fine.

In terms of policy, the question is central.

Were inflation and interest rates both 8% in Japan, there is no way in hell that the country would have borrowed 200% of GDP, even if in theory the inflation was amortizing the balance and created ‘equivalence’, because near term interest expense could be as high as 16% of GDP.

Similarly, if interest rates went from 0% to 2% in Japan, near term borrowing (assuming all debt re-priced immediately) would increase from 2% to 6% of GDP. The Finance Minister, in such a case, would be in no position to talk about ‘equivalence’. He would have to resign.

Japanese politicians did not borrow 200% of GDP because they were thinking about some sort of long-term equivalence. They borrowed it 1) because western economists kept talking about boosting the Japanese economy with deficit spending — which is just nonsense with a rapidly declining workforce and decent per capita worker productivity growth; and 2) because they could. The Japanese used debt to reconcile the difference between lagging revenue increases and rapidly worsening demographics.

Thus, fiscal policy in Japan has migrated from one constrained by interest expense to one based on total borrowing capacity, under the implicit assumption that interest rates would never rise and thus, that 200% debt to GDP was, as long as it could be refinanced, free money. There is no equivalence here. Just massive principal-agent problems and the political path of least resistance.

If you project out Japan’s demographics and fiscal situation, all that debt does remain free if nothing goes wrong. If anything goes wrong, the Japanese economy blows up in the most spectacular way. That’s not ‘equivalence’ as I think of it.

We can project these same issues onto the US. It is absolutely astounding that some of the wealthiest US states — Connecticut, New Jersey, Illinois — are in dicey financial shape. In Illinois, pension expense is now 25% of the budget. Was this a surprise? No. We’ve known about these pension problems for decades, but politicians over and over were willing to garner political favor with promises which would mature once they had left office. There was no equivalence, just short-term expediency.

We may be seeing this replayed on the national level. If you believed interest rates would rebound sharply, the Republicans would likely not have passed the tax cuts they did. Implicit in the Republican plan is the continuation of interest rates at some low level. Now, the demographics suggest that this assumption will hold up; indeed, interest rates could easily come in under CBO projections. On the other hand, if interest rates will behave as they did in, say, prior to 2008, then we could see something of a Kansas scenario being repeated at the national level, as rising interest rates essentially force Republicans to walk back the tax cuts in 2020-2021 time frame.

Thus, it is all well and good to be ‘agnostic’ about demographics and interest rates. This is, however, akin to a pilot telling his passengers that he is not sure what direction the plane is flying in, but surely it will land somewhere. For most of the passengers, where the plane lands matters. There is no ‘equivalence’.

24. January 2018 at 14:46

The notion that population growth caused the “Price Revolution” of late C15th to mid C17th is alive in historical scholarship.

These folks have apparently never heard of the C19th.