The increasing popularity of NGDP targeting

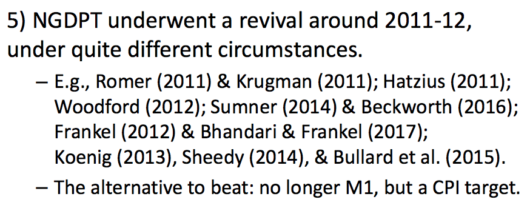

There seems to be an increasing groundswell of support for NGDP targeting. At the recent AEA meetings in Philadelphia, David and Christina Romer presented a paper that endorsed the concept. A couple days later Larry Summers touted the idea at a Brookings Conference on monetary policy. At the same conference, Jeffrey Frankel presented this slide:

Sam Bell directed me to a copy of the Fed minutes from 1995, where Lawrence Lindsey endorsed the idea:

Sam Bell directed me to a copy of the Fed minutes from 1995, where Lawrence Lindsey endorsed the idea:

…one of the things we all taught in economics was that, if we have one instrument, we can only work with one target. I don’t think it necessarily follows that the target should be price inflation. I think it should be nominal GDP, and I believe that is somewhat in line with what Governor Yellen said. But once we pick nominal GDP as our objective function, it begs a second question that has to be answered. It is that a nominal GDP target probably has to be consistent with some desired level of inflation. So, having this process and having Congress tell us some desired level of inflation, I think is probably good. But our target should not be the desired level of inflation; our target should be nominal GDP.

Lindsey is a leading candidate for the position of vice chair of the Fed:

Other names linked to the position at the time include former Fed Governor Lawrence Lindsey, head of an economic advisory firm, and Mohamed El-Erian, a columnist for Bloomberg View and chief economic adviser at Allianz SE, Pimco’s parent company. Neither could be immediately reached for comment on Monday.

Unfortunately he does have one downside:

In contrast to Chairman Greenspan, Lindsey argued that the Federal Reserve had an obligation to prevent the stock market bubble from growing out of control. He argued that “the long term costs of a bubble to the economy and society are potentially great…. As in the United States in the late 1920s and Japan in the late 1980s, the case for a central bank ultimately to burst that bubble becomes overwhelming. I think it is far better that we do so while the bubble still resembles surface froth and before the bubble carries the economy to stratospheric heights.”

I don’t think you want to point to the late 1920s as an example of why central banks should pop stock market bubbles.

(In this post I discussed El-Erian.)

Here’s another interesting slide from Frankel’s presentation:

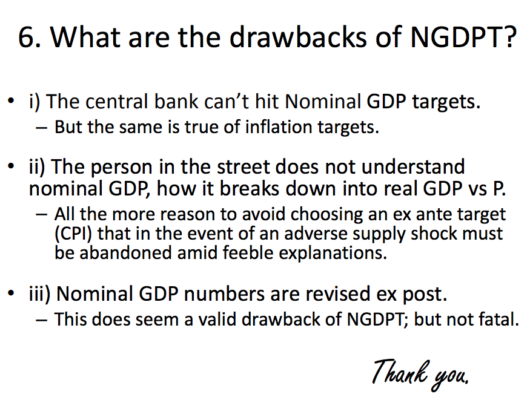

Here are a few thoughts on those three points:

Here are a few thoughts on those three points:

i. I believe the Fed can hit an NGDP target, or an inflation target. The Fed also believes that, or they would not be raising interest rates right now.

ii. I believe that people actually understand NGDP targeting better than inflation targeting. Ask 100 people back in 2010 why the Fed was trying to raise the inflation rate. Ask them why the Fed thought it was a good idea to raise the cost of living for American citizens at a time when they were struggling with high unemployment and heavy mortgage debt. I bet less than 3 out of 100 could answer the question. Then ask them why the Fed might want to raise America’s total national income during a deep recession.

iii. I wonder if the data revision issue implies that we should be targeting something like total labor compensation. Am I correct in assuming that this variable is revised less significantly than overall NGDP? It might also correlate better with labor market stability.

HT: Sam Bell, Scott Freelander, Tyler Cowen

Tags:

11. January 2018 at 23:52

All hail NGDP LT!

I see the weaknesses of NGDP targeting as–

1. There is a constant bias in modern central banks to being too tight. So a target will be selected, but one that suffocates the economy.

2. Even if a good target is selected, the central bank will be too timid to use the tools it needs to reach the target. For example, helicopter drops or buying foreign bonds.

12. January 2018 at 02:46

Is it too early for us to guess which Central Bank will adopt NGDP Targeting first?

😁😁😁

12. January 2018 at 02:54

The “anything but inflation targeting is too hard for the average joe” spiel is a terribly patronizing view. How that can be considered a valid objection really shows how conservative central banks can be.

12. January 2018 at 06:43

The likelihood of data revision is no problem if the target is not NGDP but rather *the market forecast* of NGDP.

12. January 2018 at 07:21

About point iii: I think that a total labor compensation would be good.

Here’s what total weekly wages looks like (private sector):

https://fred.stlouisfed.org/graph/?g=huhN

The data for production and nonsupervisory workers goes back to 1965:

https://fred.stlouisfed.org/graph/?g=huij

A few advantages:

(1) Wages information is “high-frequency” data. It’s collected once a month and published within a week, rather than once-per-quarter, with a month-long delay. Higher-frequency data with less lag would help decision-making, whether these decisions are made by a committee or the market.

(2) It’s highly correlated to NGDP anyways. It’s also partly “insulated” from commodity-based shocks.

(3) The public would certainly understand the concept.

(4) It’s not affected by “leprechaun economics”.

(5) Getting even higher-frequency data (say weekly data) for wages is probably easier than for (n)gdp.

(6) From the two graphs above, tight and loose monetary policy can be identified really easily, as deviations from trend. For example, there is absolutely no ambiguity that total wages were well below trend by May 2008, well before other indicators barked. Likewise, the loose stop-and-go policy of the late-60s and 70s is obvious. It also shows that since 2010, the Fed has imposed a super-great-moderation (the year-over-year data is remarkably stable, but at a lowish rate).

Some issues:

(1) How to deal with mixed-income and self-employment?

(2) As mentioned in the weblog post, how to deal with revisions?

12. January 2018 at 08:17

LK, Excellent comment. The BEA national income accounts report total labor compensation; they may impute a certain amount of labor income to the self-employed, I’m not certain.

That data is quarterly, but may also be available at higher frequencies. I’m curious as to whether big GDP revisions are in other categories (profits, rents, depreciation, etc.)

12. January 2018 at 08:48

As long as they’re level targeting rather than chasing y/y percentages, why would the revisions be a problem? Simply adjust the level target by the same amount to maintain the same target growth. It’s not the target that matters for guiding their near-term monetary activity; it’s the nominal growth required to move from the last measurement to the new target.

12. January 2018 at 11:45

Total labor compensation seems like it would be one of the easiest targets to sell politically.

12. January 2018 at 12:10

Randomize and Philo

Revisions are a problem for contracts. The inflation indices are not revised in part because many contracts–including TIPS–are based on inflation indices. This is important if we want well functioning ngdp or ncomp (nominal labor compensation) prediction markets.

12. January 2018 at 12:51

I assume total labor compensation doesn’t have imputed rent since it doesn’t have capital accounts. That’s a win over NGDP. Although I understand the purpose of imputed rent, it’s still weird to me.

12. January 2018 at 14:08

The NIPA accounts split out proprietor’s income without any judgement made about capital vs. labor.

https://www.bea.gov/iTable/iTable.cfm?reqid=19&step=2#reqid=19&step=3&isuri=1&1921=survey&1903=53

For Q3 2017, total compensation of employees was $10.3tr and proprietor’s income was $1.38tr. Even some small percentage of rental income ($747bn) and corporate profits ($2.2tr) are returns to labor rather than capital. NIPA appears to account for stock option compensation, but many successful business owner’s made a nominal “investment” at incorporation.

The BLS, as opposed to the BEA with NIPA, does make an estimate of capital vs. labor for proprietor’s compensation. The BLS makes it impossible to find simple, nominal total compensation (as in, trillions of nominal dollars). Everything is based on hourly rates or indexed to 100 from some date. At least it’s beyond my ability to walk back the BLS data to a nominal total comp. measurement including proprietor’s income.

FWIW, there seems to be general rule of thumb of 2/3 of proprietor’s income going to labor.

As far as revisions, they’re really small for NIPA’s compensation and proprietor’s accounts. Highest revision was $20bn or 0.2% of compensation account for Q4 2015. Other revisions were <0.1%.

12. January 2018 at 14:52

OT – about monetary offset.

https://www.ft.com/content/3ffd79c8-f71d-11e7-8715-e94187b3017e

12. January 2018 at 18:50

OT but related and a laugh and a conundrum: We are told that “expectations” are very important. The Fed must signal and then the public will “expect” certain levels of inflation.

But!

For about the last 40 years, conventional US macroeconomists (and the bulk of the financial community) have been predicting (nearly hysterically at some junctures) higher inflation and interest rates ahead, even runaway inflation. They expected, expected, expected, expected, expected higher interest rates and inflation.

Great Expectations! (sorry, Dickens)

The Inflation Bogeyman was not just knocking at the door, he had kicked it down and was on the threshold! Armed and loaded for bear! And mean!

Instead, inflation and interest rates have gone down since 1980 (in general).

So do expectations matter?

13. January 2018 at 06:57

Ben Cole,

It’s only the monied bets that matter. Talk is cheap. Bryan Caplan perhaps best makes this point.

Even fools who actually bet their money help markets by creating arbitrage opportunities.

13. January 2018 at 07:41

Have you ever talked Economics with the general public?

If readers of this or any economics blog want to imagine the economic literacy of “the person in the street”, try to remember your knowledge of economics when you were 12 years old. Real people devote 1000 times the mindshare to the NFL, The Bachelor, NASCAR, the Kardashians, etc., than they devote to Economics. (Maybe 10,000 or 100,000)

“The person in the street” is not even aware of the distinction between Nominal and Real GDP. I contend they understand Nominal GDP far better than they understand Real GDP because NGDP is what is intuitive at first blush, without thinking. A little study is necessary to understand that NGDP can be split into two components, more study than the person in the street has done.

If you don’t believe, ask a few random people at Wal-Mart to describe the difference between Real GDP and Nominal GDP.

13. January 2018 at 08:41

@ L K Breland:

I don’t get your point. The “NGDP” prediction market that the Fed uses for its targeting could be based on the initial government estimate of NGDP; perhaps that would be more convenient than using a prediction market based on the final revision–or on the first revision, etc.–though those would also be possibilities. If the Fed is going by first estimates, revisions would be irrelevant; alternatively it could go by the final, revised estimate, which would delay settlement of the contract but would accommodate revisions.

Admittedly, putting such stress on the government’s estimates might corrupt the process of estimating; that’s my biggest worry about “NGDP targeting.”

13. January 2018 at 12:10

Philo

“Admittedly, putting such stress on the government’s estimates might corrupt the process of estimating; that’s my biggest worry about “NGDP targeting.”

Mind you, CPI (or PCE inflation) targeting faces the same challenge. TIPS, inflation-based derivatives and some wage contracts depend on government estimates as well. Arguably, generating inflation indices involve more assumptions than generating wage data.

That said, you are right that the revision issue is not a huge barrier. Nngdp/ncomp/nwage prediction markets and the Fed simply need a consistent set of rules. While this may seem like a conceptually trivial issue, it’s actually the type of nuts-and-bolts issue that worries the finance people, including those at the Fed and Treasury. I.e. the same people who were against zero-interest Fed Funds rates because they were worried about money-market funds.

13. January 2018 at 14:26

Todd,

I’ve had a decent number of conversations with “people on the street.” I wouldn’t give them too much credit. But they also see some real-world effects, especially if they manage businesses and revenue for cyclical industries.

Why do their businesses have lower revenue? Well all the other businesses and employees have lower revenue. It becomes a self-fulfilling prophecy in isolation. The Fed printing money is an outside force to stop the cycle.

Same is true of *increasing* revenues being a self-fulfilling prophecy to push up prices and wages, requiring the Fed to destroy money. The public doesn’t see the linkage between price inflation, wage inflation and revenues. As Krugman says, a person thinks if I get a 4% raise its my hard work and intelligence but if I see 2% higher prices, it’s monetary debasement.

13. January 2018 at 14:37

LK,

Under level targeting, revisions get added in later anyway. If there is a Futures market, then payouts can be based on original levels. If you were long NGDP for Dec. 2017 and it gets revised upward three months later, then them’s the breaks. If you were also long NGDP Mar. 2018, then you get more money from that revision.

To be blunt, revisions are kind of a dodge to questioning the old, Medeival guild sort of monetary policy. Demanding absolute precision of level targets doesn’t hold up considering the extreme imprecision of current tools.

On a side note, Bernanke did institute IOER for money market funds and bank accounts to not have to charge fees. The contortions never made sense. If tri-party repos now had negative haircuts, what else are the pension funds going to do with the money? Invest it in riskier securities? For 2008, that sounds like a feature, not a bug.

13. January 2018 at 22:02

Todd, You asked:

“Have you ever talked Economics with the general public?”

Obviously.

In addition, I taught economics for more than 30 years. I think I have a pretty good idea how average people think about these concepts.

13. January 2018 at 22:07

Stock market gained 7.8 Trillion dollars in market value 2017

4% economic growth in 4th quarter

Lowest level of claims for unemployment benefits in 44 years

Black unemployment rate is lowest (6.8%) on record

14. January 2018 at 04:39

Benjamin Cole said: I see the weaknesses of NGDP targeting as–

1. There is a constant bias in modern central banks to being too tight. So a target will be selected, but one that suffocates the economy.

How old is this guy (an armchair economist)? The “bias” is in the monetary transmission mechanism itself.

14. January 2018 at 16:42

Unfortunately I am the same age as Scott Sumner.

I too think the present Rube Goldberg-on-LSD design monetary mechanisms are kooky.

Open market operations and IOER and reverse repos and twists and interest rates and FOMC secret meetings. QE then de-QE.

Would not simple and understood helicopter drops work better and be more transparent? You know, the democracy thing?

14. January 2018 at 17:48

On the revision issue, it seems to me that Scott’s “guardrails” approach takes care of this problem. Am I right?

15. January 2018 at 06:08

“In addition, I taught economics for more than 30 years. I think I have a pretty good idea how average people think about these concepts.”

A Bentley econ students would not strike me as a good example of an “Average Joe”. As poor as their initial economic judgment is, it’s probably still ahead of that of the average person.

16. January 2018 at 04:35

Lucas, yes, any approach using markets to look forward will deal just fine with revisions. Instead of being able to settle the one year ngdp future in, well, one year, we’ll just settle it in two years after all revisions have been done.

There’s no problem with financial institutions holding those contracts on their balance sheets for a bit longer. Especially since they will be very low risk.