What if we let the inflation genie out of the bottle?

Ryan Avent has a long and characteristically thoughtful post on the recent debate over global stagnation. He focuses on the views of Paul Krugman, Ben Bernanke and Larry Summers, three intellectual heavyweights. In the end I think Ryan’s a tad too polite, although maybe that’s my own frustration showing through. After all, these aren’t just any three economists; they are two of the most influential policymakers in recent years, and the world’s most famous economic pundit.

Here’s my problem. After nodding in the direction of inadequate monetary policy, Ryan basically accepts the framing of the demand deficiency debate—it’s all about saving/investment imbalances. But as Ryan himself acknowledges, that’s only a problem because monetary policy is not behaving normally:

Normally a central bank would try to fix the imbalance between saving and investment by reducing interest rates (which should discourage saving and encourage borrowing). But in a weak enough economy with low enough inflation the interest rate needed to balance saving and investment might become negative””maybe even really negative. Given the difficulty of achieving a negative nominal interest rate, the central bank might find it hard to push an economy out of that sort of trap once it fell in.

Ryan understands (but doesn’t mention in this post) that one way to fix this problem is by raising the inflation target. Many economists (including Krugman) have recommended raising the target to 4%. In my view 3% would be plenty high for the US.

So why don’t we do this? I can’t imagine that any serious economist believes that the harm done by an extra 1% in fully anticipated inflation is worse than the damage (supposedly) done from decades of secular stagnation. One answer is that there are better alternatives, like NGDPLT. That’s true, but we are also not adopting those better alternatives. Another is that “using monetary policy” would create bubbles. But we always use monetary policy; not using monetary policy is not an option. What Larry Summers actually objects to is having the private sector allocate increased investment spending, at a time he prefers more public investment on infrastructure.

And yet Summers is obviously not typical of the opponents of higher inflation, who are most often on the right. The argument that I hear most frequently is that 3% inflation would “let the inflation genie out of the bottle.” We saw in the 1960s that once we let inflation rise to 3%, it rose to 4%, then 5%, then eventually 13%.

And yet . . . prior to the 1960s the Fed had no experience in inflation targeting. Now they’ve shown they can keep inflation close to 2% or slightly lower for as long as they wish. They’ve learned the Taylor Principle. I know, you are thinking; “Still we can’t really know the effect of a higher inflation target until it’s been tried.” Don’t be a stupid American, the type who pays no attention to the rest of the world.

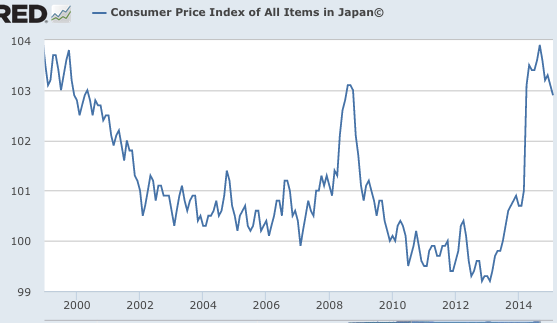

A few years ago the Japanese raised their inflation target from “stable prices” to 1% inflation. Then at the beginning of 2013 they again raised their inflation target to 2%. And what did the mean, scary Japanese inflation genie do once it got out of the bottle? Well the Japanese CPI was about 99 at the beginning of 2013, and now it’s about 103. I’ll let you do the math.

More recently the ECB has sharply depreciated the euro. The Fed is planning on raising interest rates soon, which means they don’t see any demand deficiency—mostly because the Bernanke Fed did more monetary stimulus than the ECB in previous years. Monetary policy works at the zero bound.

Here’s how central bankers envision the scary Japanese inflation genie:

And here’s what it actually looks like:

PS. I do not favor raising the inflation target, I favor NGDPLT. But if the choice is between decades of “demand deficiency” and/or billions spent on Japanese style bridges to nowhere, and 3% inflation, I’ll take my chances with the scary inflation genie.

PS. I do not favor raising the inflation target, I favor NGDPLT. But if the choice is between decades of “demand deficiency” and/or billions spent on Japanese style bridges to nowhere, and 3% inflation, I’ll take my chances with the scary inflation genie.

PPS. Perhaps I’m not afraid because as a child I watched the TV show “I Dream of Jeannie.”

Tags:

4. April 2015 at 14:50

Great post Scott. Hell, I’d be ok if the Fed demonstrated it was serious about its 2% target.

4. April 2015 at 15:00

Scott, I know you don’t think (and I agree) that interest rates aren’t a good metric for judging monetary policy. But I was reading Ben Bernanke’s new blog on why interest rates are so low, and he was talking about how central banks have tried to raise rates only to steer into a state of disequilibrium above the Wicksellian rate.

While monetary policy cannot be *judged* via interest rates, is this still a valid way of enunciating the problem? Say short-term rates rise due to monetary tightening via the liquidity effect, is saying “it was out of place relative to the Wickesllian equilibrium rate” essentially the same as saying “money was too tight and nGDP growth wasn’t strong enough”?

Or am I missing a fundamental difference between how you describe the problem and how Bernanke describes the problem?

4. April 2015 at 15:09

Excellent blogging.

But to obtain the higher IT will require an immediate return to QE.

There is more good news. The US economy is far less inflation-prone than in the 1970s. Whole industries have been price-deregulated, such as transportation and communications and finance.. Labor unions have been all but eliminated. International trade is about a third of GDP instead of less than 10%. The minimum wage is much less. Top marginal tax rates are much lower.

The question is how much stimulus and how much real growth would it take to get to 3 percent inflation—it would take a lot of prosperity to get there.

By the way, the average rate of inflation from 1982 to 2007 was about 3 percent and the average rate of real growth in GDP was also 3 percent.

There are reasonable fears in life, and then there are monomaniacal phobias.

4. April 2015 at 18:52

I believe that recent inflation is mostly VAT increase (graphs at link):

http://informationtransfereconomics.blogspot.com/2015/03/japan-inflation-update.html

If you adjust for the two VAT increases (1997 and 2014) the price level seems to have a smoother trend.

4. April 2015 at 19:44

“Another is that “using monetary policy” would create bubbles. But we always use monetary policy; not using monetary policy is not an option.”

Lowering rates and asset purchases fuel bubbles. Heli drops stimulate by increasing monetary wealth of recipients while maintaining a higher rate therefore not facilitating bubble creation as much.

4. April 2015 at 20:42

Money is neutral and super-neutral, except in extreme (hyperinflation) cases. Hence, printing money and buying commercial paper is like pushing on a string. Banks are well below their legal limits on creating loans from their reserves (from an economist on the net) so, why would the Fed giving more cash to the banks via high-powered solve anything? It won’t. Already banks cannot lend out the money they have now.

The only way (besides government fiscal policy, which is wasteful) to generate inflation is for the Fed to do what the Weimer Republic did in the 1920s, to get rid of their war reparations debt: crank up the printing presses so hot, like our own B. Cole wants, that hyperinflation results (despite money super-neutrality, hyperinflation is the exception that proves the rule). Is that really Sumner’s hidden wish? I wonder sometimes. And BTW Sumner was roughly a teenager, not a “child”, during the September 1965 to May 1970 period that I Dream of Jeannie ran.

5. April 2015 at 03:28

“Banks are well below their legal limits on creating loans from their reserves (from an economist on the net) so, why would the Fed giving more cash to the banks via high-powered solve anything?”

First, just because banks are well below their legal limits on creating loans does not mean that with fewer reserves they would still create as many loans as they are doing today.

Second, there are reasons to believe that the Fed was more interested in puffing up the base than in raising nominal income. (While they did create lots and lots of reserves, they took steps – eg IOR and “open-mouth operations” to ensure that money stayed in banks.

5. April 2015 at 03:41

Scott, am I crazy to see a contradiction between this post and your last one?

In the last post, you seem to argue that for various supply side reasons the best we are going to do is about 1% growth, and (with inflation slightly under 2%) 3% NGDP growth. It seems like you are (implicitly) arguing that, yes, the Fed could have 5% NGDP growth if it wanted, but that would just mean 1% real growth with 4% inflation.

In this one, you are back to pointing out the benefits of NGDPLT or even (though it would be worse than NGDPLT) a higher inflation target.

NGDP growth has been fairly stable at about 4% for a couple of years now, hasn’t it? Now the hypermind forecast might be an indication that monetary policy is tightening. Maybe *that* is behind the softer employment report?

5. April 2015 at 06:49

Ashton, It’s valid to talk about the difference between markets rates and the (unobservable) Wicksellian rate, but not useful.

Ben, Delaying the rate increase would probably be enough.

Jason, It’s about 1/2 VAT, which of course strengthens my point.

CMA, I know of no evidence that lowering rates fuels bubbles, which tend to occur when rates are rising (1928-29, 1987, late 1990s, 2004-06.)

Ray, I was 10 years old, I guess I should have said I was “roughly a teenager.” Yep, you caught me.

Michael, With NGDPLT we would have had a much faster recovery.

5. April 2015 at 16:22

Scott Sumner

“I know of no evidence that lowering rates fuels bubbles, which tend to occur when rates are rising (1928-29, 1987, late 1990s, 2004-06.)”

Would you agree that a higher interest rate during those times you mention would of generated less credit and bubbles? How much less is hard to know exactly but at least marginally less bubble formation would have to be the result of higher rates.

5. April 2015 at 19:41

The Atlanta Fed has produced a “Sticky-Price CPI” that it says is sensitive to expectations in future price changes.

Here’s a bit from the explanation of it, in Part 2 of a three-part series on the CPI, cost of livings and differences between…

http://macroblog.typepad.com/macroblog/2014/06/torturing-cpi-data-until-they-confess-observations-on-alternative-measures-of-inflation-part-2.html

And here it thing itself, and its crystal ball view of the future

…

https://www.frbatlanta.org/research/inflationproject/stickyprice/

6. April 2015 at 05:32

CMA, You said:

“Would you agree that a higher interest rate during those times you mention would of generated less credit and bubbles?”

Do you mean a higher i-rate or a tighter monetary policy? Those are two different things. After 2000 the Fed cut rates sharply and stock prices FELL—the opposite of the bubble prediction.

Thanks Jim, That looks interesting.

6. April 2015 at 10:10

Brazil adopted IT in 1999, the year the currency was floated and we had 9% inflation, the plan was to take the target down to 3.0% with 1% tolerance. But when the left wing PT party took over in 2002, the scrapped the plan and settled with 4.5% target and 2% tolerance. Over time inflation grew from 4.5 to 6.0% – 6.5% (it’s been in this range for a few year now), and in 2015 it is expected to breakout from the tolerance band. Brazil has a lot of structural problems, I know, but if the credibility issue can be examined independently from other issues, the Brazilian experience has not been that good …

6. April 2015 at 13:57

“But as Ryan himself acknowledges, that’s only a problem because monetary policy is not behaving normally:”

No, fiscal policy is also not working normally. “Normally” when the borrowing rate falls more projects with positive NPV appear and this should “normally” lead to more deficit spending until rates rise. Instead in the UK, Europe and the US, spending on activities with current costs and future benefits was reduced.

7. April 2015 at 06:53

Thomas, That’s reasoning from a price change. It depends why rates have fallen. You can’t assume that more investment projects are feasible unless you know whether rates fell because savings shifted right or investment shifted left.

7. April 2015 at 07:28

“Thomas, That’s reasoning from a price change. It depends why rates have fallen. You can’t assume that more investment projects are feasible unless you know whether rates fell because savings shifted right or investment shifted left.”

Yes. The lower rate would obviously reduce costs and lower the discount rate in the NPV calc, but one can’t assume that the benefits of the project remained static or that there were an abundance of projects just below the NPV cutoff prior to the rate change.