There are many different types of superintelligence. Some people understand quantum mechanics. Some people are really good at chess. Some people can read Finnegan’s Wake.

[I’m tempted to say, “Some people understand supply and demand

Scott Alexander is really, really good at analysis. So good that he’s become famous for engaging in this activity, with a cult following all over the world. (In recent years, the new people I meet in Orange County are largely through Scott Alexander meet-up groups.)

Thus it would be interesting to see what would happen if Alexander took a deep dive into the Covid origins debate, and looked at all of the evidence that’s been presented by both the Lab Leak and Zoonosis advocates.

Now he’s done so. First in a post that looked at a highly publicized debate between the two sides, and now in a follow-up post that dealt with a wide range of comments on his first post. (For those who don’t know, his comment sections are very long and full of high quality observations. If the objection is not in his comment section, it’s probably not worth considering.)

In the end, Alexander comes down pretty close to where I am:

For now, I’m still at 90-10 zoonosis.

And like me, he gets frustrated with the game of whack-a-mole played by Lab Leak proponents:

I know this comments post won’t be the end of the story. I know that (just as with every other one of my posts, I’m not blaming origins debaters in particular here) someone’s going to go “Sure, Scott confronted 489 arguments. But he failed to confront the strongest argument against his case – this one obscure article in a Nepalese journal that nobody except me has ever heard of. That means he’s a bad-faith actor strawmanning everyone he disagrees with!” I know that someone will find some detail I’m wrong about and spam it all over Twitter with “Scott didn’t realize that an 91Q mutation is different from a ZY6 mutation, how can you ever trust anything he says?” And I know that next month, someone will come up with another SMOKING GUN! – and if I don’t respond to it immediately they’ll say I’m scared and know I’ve lost and am refusing to admit I’m wrong out of sheer stubbornness, and twist some quote of mine to show I’ve admitted I’ve changed my mind.

You need to devote a considerable period of time to the debate if you truly wish to become informed on this issue. Alexander’s two posts are a good place to start.

I occasionally read some really smart bloggers who view both lab leak and zoonosis as being roughly equally probable. I respect their views, as that likely means they didn’t waste enormous portions of their life taking a deep dive into this debate like I did. Good for them. I suspect that if they read Alexander’s two posts carefully, they’d switch their views toward strongly favoring zoonosis—the evidence is pretty strong in that direction.

A couple years ago, commenters raked me over the coals for refusing to admit what they thought was obvious—that Covid came from a lab leak. They claimed I was stubbornly refusing to admit the obvious out of some sort of strange loyalty to the CCP (despite the fact that I said lab leak is a danger worth worrying about, and despite the fact that I severely criticized the CCP at the beginning of the pandemic, and despite the fact that zoonosis is far worse for China’s reputation than lab leak, which explains why the CCP has vigorously tried to cover-up the zoonosis evidence.)

No doubt these commenters will show up here and apologize for their slander against my character.

Just kidding!!

PS. I enjoyed this comment, in reference to a picture of WIV scientists:

This is the Wuhan Institute of Virology’s coronavirus research group, out for a team dinner at a local restaurant on January 15th 2020 (ie a month after the pandemic started). This isn’t the most rational probabilistic evidence in the world. But we’ve already seen people take the rational probabilistic evidence twenty different directions. So let’s ask the same question Peter did – do these look like people who secretly know they just started the worst pandemic in modern history?

If they secretly knew they’d just started the worst pandemic in modern history, wouldn’t they at least be wearing masks?

Like Alexander, I don’t see the picture as being definitive evidence, rather it’s a reminder that these are real people. When I read lots of recent western commentary on China, I get the impression that the Chinese people are viewed as some sort of totalitarian cyborgs. But when I visit China and talk to people, they seem kind of like Americans. I’m slightly more persuaded by a western scientist that met the WIV people at a conference at the end of 2019, and reported that their mood seemed completely normal. Scientists aren’t like lawyers—they’re pretty transparent.

I also believe that people underweight the fact that the Chinese scientists clearly thought it was zoonosis in the early stages of the pandemic, before the CCP told them to keep quiet and began pushing alternative theories.

People who’ve never been to China often have this weird idea that the CCP is omniscient, and that nothing happens in China without the CCP knowing about it. China is different in some respects, but nowhere near as different as many of you assume. Like the US, it’s a vast and endlessly complicated place.

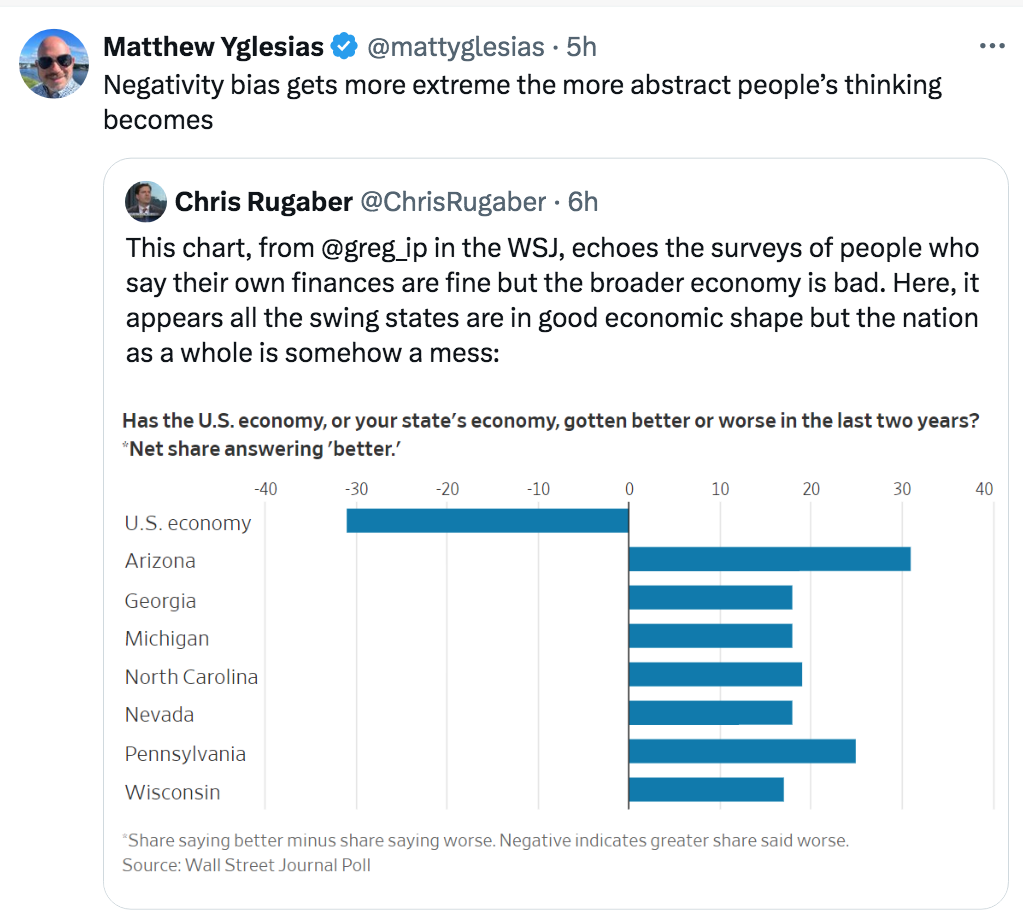

We’ve reached the point where Biden administration officials, Democrats, and pro-Biden columnists are tearing their hair out, furious that the electorate perceives the economy as being subpar. But if you look in the right places, the economic frustration makes perfect sense — and those right places include grocery prices since before the pandemic, the number of new jobs that are part-time jobs, the current high gas prices and likely summer price hikes, how inflation counteracts the good recent run of the stock market, and how many people owe more in car payments than the worth of their automobiles. Americans measure the economy by a lot more than just the unemployment rate, and no amount of wishing, ranting, or berating is going to get them to change their minds about how they perceive their household finances.

I hope you see the problem here. Americans rate their “household finances” as good, it’s the overall economy they view as poor. No amount of ranting and berating from Jim Geraghty will change that fact. Here’s Axios:

By the numbers: 63% of Americans rate their current financial situation as being “good,” including 19% of us who say it’s “very good.”

Neither number is particularly low: They’re both entirely in line with the average result the past 20 times Harris Poll has asked this question.

The survey’s findings were based on a nationally representative sample of 2,120 U.S. adults conducted online between Dec. 15-17, 2023. (More on the methodology.)

Americans view the economy as poor partly because of the inflation and partly because they hate Biden. Americans view their personal finances as good because their incomes have generally risen faster than the cost of living since the pre-Covid period. (Comparisons with early 2021 are meaningless, as the data was heavily distorted by Covid.)

PS. Biden’s economic policies are really bad, but for reasons that have nothing to do with the current state of the economy.

PPS. Trump has a 6-part plan to bring down inflation:

1. Favors NIMBY policies to prevent housing construction in the suburbs.

2. Expel all the illegal workers that pick our food and provide other key services.

3. Put heavy tariffs on imported food and other goods.

4. Have Medicare do less negotiation of drug prices.

While several states have banned abortion, a bunch of other states have made it easier to get medication abortions and otherwise reduced restrictions with the result that there were actually more abortions in 2023 than in previous years. And abortion rights is getting more popular. A new Fox poll showed that 70 percent of the public believes mifepristone should be legal and the previously popular idea of a 15-week ban is now underwater 43-54. Abortion rights have become a millstone around the GOP’s neck, and the more people argue about this, the more they seem to be moving in favor of abortion.

As a matter of law, I agree with the Supreme Court. But as a matter of policy, I’m pro-choice.

2. I’m so glad to live in a state where pot is legal, abortion is legal, physician assisted suicide is legal, you can buy Teslas directly from the manufacturer, and lab produced meat is legal:

Lawmakers in US state capitals are seeking to stifle development of “lab-grown” tuna, pork and other animal proteins, taking a stand against a novel food technology backed by investors such as Bill Gates and Jeff Bezos.

Republicans in at least seven states have introduced legislation since the beginning of the year to ban sales or distribution of lab-grown meat, a form of edible protein cultivated from animal cells. . . .

Florida’s legislature in March sent legislation banning sales of lab-grown meat in the state to DeSantis, who in February said: “We are not going to do fake meat. That does not work.” A spokeswoman for the governor declined to comment on whether he will sign the bill.

The GOP fervently believes that every American should be free to pursue GOP-approved lifestyles.

A myriad of red flags went up throughout the quarter. First, Tesla warned its rate of growth will be “notably lower” this year, blaming interest-rate hikes that have kept its cars out of reach for many consumers even as it’s slashed prices. The company dealt with multiple disruptions at its plant outside Berlin. Musk engaged in inflammatory posting on X, turning off prospective buyers, and China’s EV market grew even more cut-throat.

I don’t have a Harvard MBA, but when most of your customers are Democrats, does it make sense for the CEO to spend all his spare time insulting liberals on Twitter, er, . . . I mean X?

Maybe he thought it would convince Republicans to buy EVs. Did Trump convince Republicans to take the vaccine?

BTW, I think Tesla is a great company. But that new pickup truck? Yikes.

But that can be worthwhile. Some 5-10% of the world’s gold production derives from pyrite. And this is likely to increase. According to estimates by McKinsey, a consultancy, 24% of the world’s gold reserves are “refractory”—meaning the gold must be yanked from the clutches of some mineral, in most cases pyrite.

5. I’ve been dismayed to see the GOP become an increasingly pro-Putin party. Previously, I attributed this to Trump. But a GOP Congressman suggests that extensive Russian propaganda also plays a role. (If I didn’t block lots of Russia trolls, this blog’s comment section would be almost entirely dominated by pro-Putin posters.)

6. I thought that Russia’s invasion of Ukraine might cause a few anti-China people to rethink their views on the “real enemy”. Unfortunately, it did not. And according to The Economist, things are even worse than I imagined:

To get involved directly, says Mr Biden, would be “World War III”. He has refused calls to impose a no-fly zone over Ukraine, act as the intermediary for Polish MIG-29 jets or even supply American-made Patriot anti-aircraft batteries. . . .

Mr Biden’s caution in Ukraine contrasts with his almost careless talk about defending Taiwan against China. Last year Mr Biden said America had a “commitment” to defend the island. America’s “strategic ambiguity”, whereby it promises to help Taiwan defend itself but will not say whether it would intervene directly, has become less ambiguous.

So we should not risk WWIII with nuclear armed Russia, but we should risk WWIII with nuclear armed China? I agree with Biden on Ukraine, but his China policy is madness. Yes, I know. Gotta defend those semiconductor factories. As George C. Scott once said, “I’m not saying we won’t get our hair mussed”.

7. Making fun of the intelligence of conservatives is like shooting ducks in a barrel. (Ditto for leftists.) But the following tweet also makes me wonder why so many conservatives wish our educational system went back to teaching the classics. Say what you will about extremists like the Taliban, at least they understand that the arts are a force for liberalization.

Hey conservative parent. Do you really want your children to read what Jesus said about how you should treat the poor refugee that shows up at your door?

(Of course Romeo and Juliet should be mixed race. My only complaint is that the two actors don’t look like children.)

8. China has been demonized for supposedly building lots of “overcapacity.” This led the US to impose high trade barriers. But as David Fickling at Bloomberg recently pointed out, the accusations are not true:

The trouble is, none of it was true. China wasn’t seeking to produce more steel than long-run demand would dictate. It wasn’t even a particularly important exporter. It wasn’t responsible for weak prices in the US. The tariffs didn’t halt a jobs decline in US metals manufacturing.

It’s bad enough that misguided steel protectionism over the past decade has served only to raise costs and reduce competitiveness for the rest of the US economy. Worse still is the way the same failed policy is now being dragged out to support far more damaging barriers on clean technology, slowing our ability to halt the rise in global temperatures.

9. The Biden administration is pursuing an “industrial policy” aimed at boosting manufacturing. Australia tried a similar policy back in the 1960s, and it failed. Here’s The Economist:

The [Australian auto] industry survived so long only because successive governments refuelled it with subsidies. GM guzzled about A$2bn ($1.3bn) before the handouts were cut by Mr Morrison’s party in 2013. Rightly so, according to a report released the following year by the Productivity Commission. It found no evidence that they had helped the wider economy, concluding that the “costs of such assistance outweigh the benefits”.

Manufacturing’s share of Australia’s economy peaked in the 1960s, in Holden’s heyday. It now accounts for just under 6% of GDP, well below the level of most other rich countries. But that has not stopped the Australian economy—and local wages—from growing faster than their peers.

Each day I get more and more depressed about the intellectual climate in America (and the rest of the world.) How often do you see people quote polls suggesting that the public believes the economy is doing poorly, as if these polls actually meant something?

Matt Yglesias directed me to this Chris Rugaber tweet:

I read another Gene Wolfe trilogy, this one about ancient Greece. Not as good as the three “Sun” series, but still enjoyable. Stefan Zweig’s The World of Yesterday was another highlight, a brilliant work of social science masquerading as a memoir. Benjamin Moser’s The Upside Down World is an excellent study of Dutch painting, and more. How good could Carel Fabritius have been? A few of his paintings remind me a bit of Velazquez. I also enjoyed Art of the Japanese Postcard. I’ve also been trying to catch up on several decades of pop music. (I’m afraid my taste is mostly stuck in 1965-80.) Lana del Rey is my newest favorite. Alvvays has some infectious pop for when you are driving, not too syrupy. Black Country, New Road is an interesting group (might appeal to Radiohead fans?) And even 2 generations later, we still have “new Dylans.” For TV, I tried The Regime and quickly gave up. It’s like Succession, but with all the good stuff removed. I recently started Ice Cold Murders, which is one more example of the now global phenomenon of complex flawed detectives with a heart of gold. I guess viewers can never get enough of this formula, although I’m getting close. At best, they are painless sociological lessons on various subcultures—in this case Alpine Italy.

2024:Q1 films

Newer Films:

Monster (Japan) 3.9 Kore-eda’s best work since Nobody Knows, and one of the best films of the past decade. Every single aspect of the filmmaking is first class, including screenplay, acting, cinematography, sound, etc.

Anselm (Germany) 3.8 An outstanding art documentary, directed by Wim Wenders. My only complaint is that I would have liked to see more on the exhibition in the Scuola Grande di San Rocco. There are interesting parallels between the style of the paintings he exhibited and the Tintoretto masterpieces in the same location.

In the Court of the Crimson King (UK) 3.7 In some ways, this is better than the Anselm documentary. But I like Anselm better as an artist, so I rate that film higher. There are some very funny sequences, as well as some deeply moving ones.

Perfect Days (Japan/Germany) 3.7 As I get older, I increasingly appreciate this sort of minimalist film. My only reservation is that at times I felt like the film was more about Wim Wender’s impeccable taste in pop music than the story he was filming.

The Movie Emperor (Hong Kong) 3.4 I generally don’t appreciate Chinese comedies, but this one was pretty effective in touching on a lot of contemporary themes. I had recently visited the Arab world, and this film convinced me that (compared to the Arab world) Hong Kong culture is much closer to American culture.

Oppenheimer (US) 3.3 Nolan’s an excellent sci-fi director, but real world science is not his forte. The visuals are fine, but didactic screenplay is tiresome. The viewer doesn’t want a three-hour history lesson on material that is already well known—or at least this viewer didn’t. This is unfortunate, as the film does have some very fine scenes. (But David Lynch’s take on the Trinity test in Twin Peaks is far superior.)

Dune 2 (US) 3.3 I saw this just a few days after it opened, and there was just one other person in the theatre. Visually impressive on occasion, but somewhat inert—lacking narrative momentum. I can’t imagine anyone wishing it to be longer. Cold and austere films can work on occasion (2001, Barry Lyndon, Stalker, etc.) but Villeneuve is no Kubrick or Tarkovsky. Heck, he’s not even Ridley Scott, as we saw with his bland Blade Runner remake.

Giannis: The Marvelous Journey (US/Greece) 2.8 He’s not among the MVP leaders (due to voter bias), but he’s probably had the best season of any NBA player. Strictly for Bucks fans.

Upgraded (US) 2.5 What happened to rom-coms? They used to be like noirs—reliable entertainment.

Older Films:

Nostalghia (Russia/Italy, 1983) 3.9 It was a privilege to see a restored version of this on the big screen. The first half in particular had one stunning image after another. This is often regarded as Tarkovsky’s weakest film, but everything he did is a masterpiece. The sublime final shot is like a Caspar David Friedrich painting come to life. Hard to see how he created it without any sort of CGI. (I beg of you, don’t watch it on TV.)

The Idiot (Japan, 1951, CC) 3.8 Who knows how good this would have been if 100 minutes had not been cut out by the studio (and lost forever.) It’s right up there with the butchering of The Magnificent Ambersons as one of the great artistic crimes of the 20th century. The film got mixed reviews, which confirms my view that many film critics are incompetent hacks. Directed by Kurosawa the year after Rashomon and the year before Ikiru, i.e., near the peak of his creativity.

The Munekata Sisters (Japan, 1950, CC) 3.7 A characteristic Ozu film from near the beginning of his greatest period.

Betty Blue (France, 1986, CC) 3.7 If Heraclitus were still alive, he’d say that no man watches the same film twice. In 1986, I thought Betty was the central character. Now I realize it was actually Zorg, who is the heart of this fairy tale for adults. I also noticed a bisexual subtext, surprising for a film that otherwise seems so heteronormative. I’m not sure how to interpret this crazy film—perhaps that living life to the fullest is a sort of mental illness. A film to make you feel both better and worse about your own (boring) life.

The Other Side of Hope (Finland, 2017, CC) 3.6 Like many Kaurismaki films, much of the humor is rather subtle. But the scene where the Finnish restaurant adopts a sushi menu is one of the laugh out loud funniest that I’ve seen in years.

Youth Without Youth (US, Romania, 2007, CC) 3.6 The critics panned this one, and I can see why. The supernatural plot is not at all believable. But the images are so astonishing that I liked the film despite its flaws. For a few moments, I was transported back to the sublime Coppola films of the 1970s.

The Yards (US, 2000, CC) 3.6 Fans of the Godfather and the early films of Martin Scorsese need to check out this excellent crime drama. It’s amusing to see James Caan essentially playing the Al Pacino role from The Godfather II. It got mixed reviews, although I’m not sure why.

I Vitelloni (Italy, 1953, CC) 3.6 This early Fellini film might seem to go over familiar ground, but that’s because it’s been copied by so many other directors.

Birth (US, 2004, CC) 3.6 Don’t believe the critics, this Jonathan Glazer mystery will stick in your mind long after the film is over. Nicole Kidman is outstanding. Glazer is an underrated director.

Godzilla (Japan, 1954, CC) 3.5 At first this seemed like a run-of-the-mill 1950s horror film. But about half way though it began to achieve a sort of tragic gravitas that was totally unexpected (at least to me.)

They Live By Night (US, 1948, CC) 3.5 In this influential noir, Nicolas Ray decides not to show the crimes being committed, focusing instead on the young lovers. I respect this choice, even though it probably made the film a bit less entertaining.

Silent Partner (US/Canada, 1978, CC) 3.5 I probably overrated this, but I’m a sucker for bank heist films with late 1970s decadence. It’s an interesting question as to which year was peak lasciviousness for western civilization. Perhaps 1977 or 1979, but I vote for 1978. It seemed like the only bra in the film was worn by a man.

Vivre sa vie (France, 1962, CC) 3.5 After 60 years, I no longer find Godard’s experiments to be all that interesting. But he’s a highly skilled filmmaker, and Anna Karina is (as usual) sublime.

10 Things I Hate About You (US, 2003) 3.4 Saw this in a theatre full of young people. Good high school comedy featuring a bunch of young actors that would soon become stars.

Little Odessa (US, 1994, CC) 3.4 Good crime drama somewhat in the style of Mean Streets, but dealing with the Russian mafia. Same director as The Yards (James Gray).

Mogambo (US, 1953, CC) 3.4 A remake of Red Dust, with Clark Gable playing the same role. Unfortunately, he’s 21 years older than in the previous version, much too old for the role. And the scenes of Africa are not very good, despite the use of Technicolor. Fortunately, John Ford is the sort of director that can turn even an unpromising film project into a quite entertaining movie.

The Moon Has Risen (Japan, 1955, CC) 3.4 Directed by a woman, with the style heavily influenced by Ozu (who co-wrote the script.)

Love Letters (Japan, 1953, CC) 3.4 Same director, but more melodramatic.

The Umbrellas of Cherbourg (France, 1964, CC) 3.4 Critics loved this film, but I have no ear for show tunes so it went right over my head. I will say that the gas station in the final scene is the prettiest one I’ve ever seen. Lots of eye candy.

Backfire (US, 1950, CC) 3.4 Not one of the classic noirs, but has a lot of very satisfying scenes. Quite entertaining, although it fades a bit at the end.

The Upturned Glass (UK, 1947, CC) 3.3 In this early film, the James Mason we know and love was not quite fully formed. Here he’s rather nervous and intense; not the calm, elegant and self-assured man I’m used to seeing in his later American films.

Drugstore Cowboy (US, 1989, CC) 3.3 The humor works better than the drama in this Gus van Sant film (as is often the case with “dramadies”.)

Starman (US, 1984, CC) 3.3 Close Encounters started strong and then ran out of inspiration. This John Carpenter film was sort of the opposite. It started rather weak—skirting the line between silly and charming. But it found a nice groove in the last 30 minutes. (To be clear, Close Encounters was much better.)

Macao (US, 1952, CC) 3.2 I never understood the appeal of Jane Russell. For a beautiful woman, she’s kind of ugly. Fortunately, the film also has Robert Mitchum and Gloria Graham. And it’s directed by Josef von Sternberg.

The Erl King (France, 1931, CC) 3.1 The images are art nouveau, a style that was already several decades in the past when the film was made. Special effects often look dated as time goes by, and this is no exception. Based on the famous Goethe poem.

Pandora and the Flying Dutchman (US, 1951, CC) 3.0 James Mason is darkly suave and Ava Gardner is radiant. So why the mediocre rating? The script is cringe-worthy, perhaps the worst I’ve ever seen in a major Hollywood production.

Code 46 (UK/China, 2003, CC) 3.0 It was filmed in what was supposed to be a futuristic Shanghai, but the Shanghai of 2003 already looks rather antique. Timothy Robbins is badly miscast—no idea what the director was thinking.

Je t’aime, je t’aime (France, 1968, CC) 3.0 This critically acclaimed film might have been impressive when it first came out, but today the time travel gimmick seems like a distraction.

Betrayed (aka When Strangers Marry) 3.0 (US, 1944, CC) Crude but fairly engrossing film noir, which comes in at just 67 minutes.

My Week With Marilyn (UK, 2011, CC) 3.0 A pleasant film with one big problem—no one can capture the magic of Marilyn Monroe. In fairness, Michelle Williams fares better than Kenneth Branagh, who falls far short of recreating Olivier’s cold intensity.

Repeat Performance (US, 1947, CC) 2.9 Think of this as the very first Twilight Zone episode. In a supporting role, Richard Basehart plays a poet who is placed in an insane asylum because he’s gay.

The Woman Condemned (US, 1934, CC) 2.8 There’s a fine line between avant garde and inept, and this interesting film noir straddles both sides of the line. Unfortunately, the print on Criterion Channel was a mess, at times almost unwatchable. Perhaps a restored version would change my view. (The New Yorker liked the film.)

The Great Sinner (US, 1949, CC) 2.6 Ava Gardener and Gregory Peck are wasted in a film that alternates between silly and pathetic. Like Harrison Ford, Peck could be charming when he was young, but became a something of a humorless bore as he aged. In this film we see both sides of his personality.

Cocktail (US, 1988, CC) 2.5 This is a fairly bad movie, but I kept watching out of fascination as to how Hollywood is able to turn junk into box office gold. It’s helps to have the world’s most charismatic actor. A good film to show to young people who wonder what the late 1980s felt like.

It’s All About Love (Denmark/US, 2003, CC) 2.2 Why did I keep watching such a bad film? I suppose it was curiosity. The film has good actors and a good director (Vinterberg), so I had a sort of morbid fascination with what would come next. Sean Penn’s performance is so bad it’s almost funny.

PS. I mentioned Moser’s book on Dutch art. Jacob Ruysdael is an underrated artist:

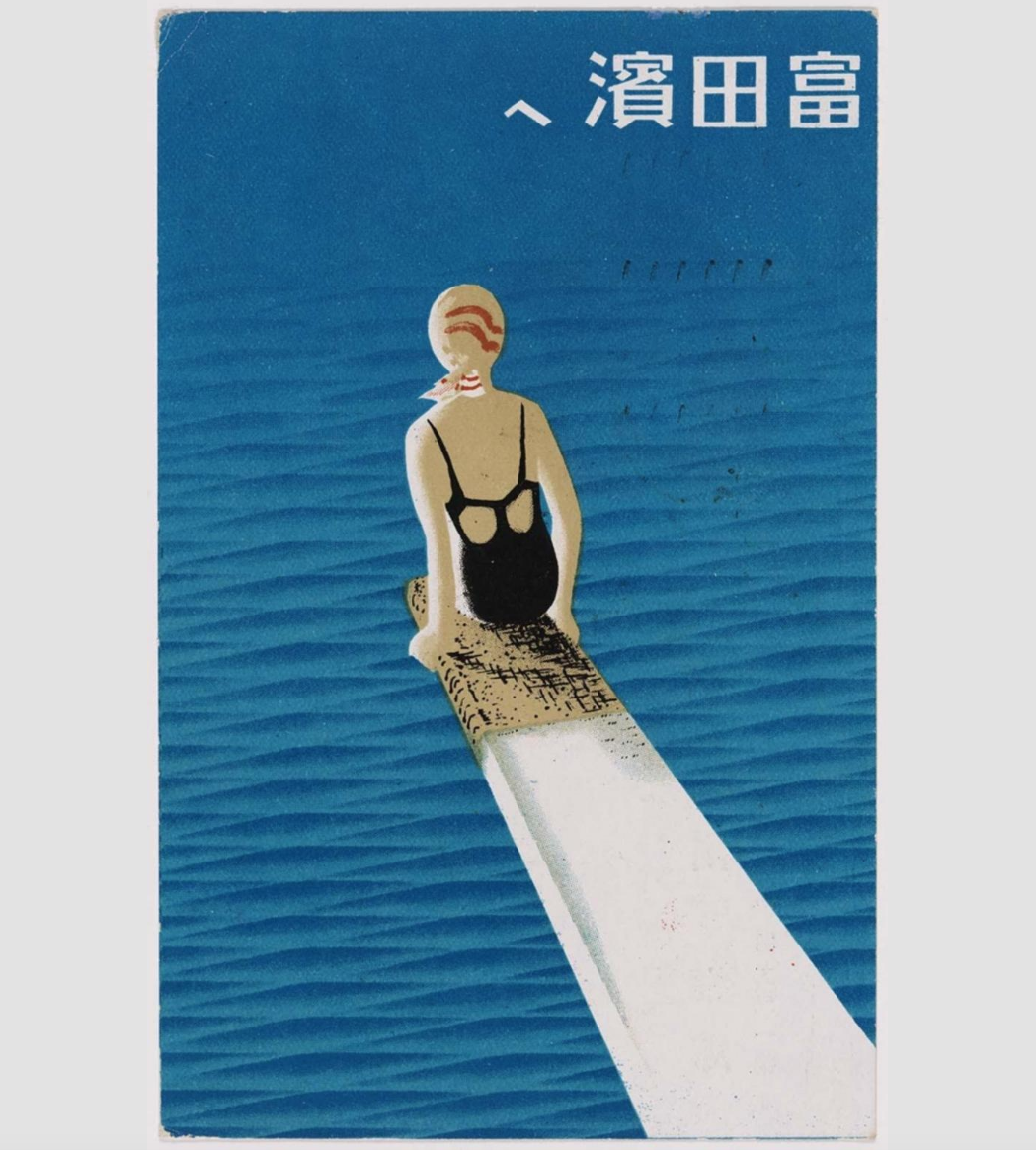

And this Japanese postcard is better than 75% of the paintings in the Louvre:

And since it’s Easter, how about a deeply religious painting:

Want something even more religious? How about the same artist in a self-portrait as Jesus:

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"ad. # 2: -no surprise here: abstract universalist principles do not work well in political practice ad # 5: - isn't that exactly the immigration pattern that is beeing experienced?..."

"So I saw a video of Swiss police strictly enforcing the law. Could that level of law enforcement make St Louis popular again?https://youtu.be/eMNhRlTX5JY?si=AuOMMPkqRR2YnXeb"

"On #3, imagine if it had been Russia. On #9, no surprise there. The Feds built a rail recently in Honolulu to alleviate traffic that doesn't even go to the..."