Here are a few articles that caught my eye:

1. Incentives matter

But on the central question—whether Uncle Sam will pay ransoms—Mr Obama was firm. American officials cannot brook the idea of funding the groups they want to destroy, and they claim that kidnappers specifically avoid taking American (and British) hostages because they do not expect a return on the investment.

There is some empirical support for that theory. In a forthcoming study of over 1,000 kidnappings by terrorists in 2001-13, Patrick Brandt, Justin George and Todd Sandler of the University of Texas at Dallas found that the number of Americans and Britons abducted each year stayed constant, whereas the totals for countries known to meet captors’ demands rose steeply. They estimate that if a non-paying government were to start offering ransoms, the number of its citizens taken hostage would jump by at least 30%.

I’d love to see the demographic breakdown of that 25%.

2. Culture matters

According to a study from the Institute of Economic Affairs, Swedish-Americans are considerably richer than the average American—as are other Scandinavian-Americans. The poverty rate of Americans with Swedish ancestry is only 6.7%, half the national average. Swedish-Americans are better off even than their cousins at home: their average income is 50% higher than theirs, a number used by opponents of the Swedish model as an argument against the shackles of big government.

Their success in America seems solidly grounded in old national virtues. They have more trust in each other and in government; they tend to obey rules (leading to many jokes about “squareheads” and “dumb blondes”). The Protestant work ethic is strong: in Minneapolis in particular, the number of Lutheran churches is striking. Scandinavian-Americans also display a keen civic sense, whether in shovelling snow or helping elderly neighbours, from which everyone benefits.

I am 1/8th Swedish and 1/8th Norwegian.

3. Good forecasters are just lucky

At times, Lord [Mervyn] King can be refreshingly frank. He is no fan of austerity policies, saying that they have imposed “enormous costs on citizens throughout Europe”. He also reserves plenty of criticism for the economics profession. Since forecasting is so hit and miss, he thinks, the practice of giving prizes to the best forecasters “makes as much sense as it would to award the Fields Medal in mathematics to the winner of the National Lottery”.

4. Never trust an America official

DEVIN NUNES raised eyebrows in 2013 when, as chairman of a congressional working group on tax, he urged reforms that would make America “the largest tax haven in human history”. Though he was thinking of America’s competitiveness rather than turning his country into a haven for dirty money, the words were surprising: America is better known for walloping tax-dodgers than welcoming them. Its assault on Swiss banks that aided tax evasion, launched in 2007, sparked a global revolution in financial transparency. Next year dozens of governments will start to exchange information on their banks’ clients automatically, rather than only when asked to. The tax-shy are being chased to the world’s farthest corners.

And yet something odd is happening: Mr Nunes’s wish may be coming true. America seems not to feel bound by the global rules being crafted as a result of its own war on tax-dodging. It is also failing to tackle the anonymous shell companies often used to hide money. The Tax Justice Network, a lobby group, calls the United States one of the world’s top three “secrecy jurisdictions”, behind Switzerland and Hong Kong. All this adds up to “another example of how the US has elevated exceptionalism to a constitutional principle,” says Richard Hay of Stikeman Elliott, a law firm. “Europe has been outfoxed.”

I can’t believe the Europeans actually trusted us. Reminds me of those naive conservatives like Ann Coulter who thought him Trump was sincere, and then were outraged when he picked a VP who doesn’t agree with his stated views on the key issues.

5. Piketty is just as left wing as I claimed

The heart of the complaint is that a Socialist government, meant to be the guardian of workers’ rights, is pandering to corporate bosses by dismantling them. Worse, goes the charge, it is making the disingenuous claim that this will help employers create jobs. “Who could possibly believe that making redundancies easier will create jobs?” reads a union flyer handed out at the rally. “Thomas Piketty agrees,” says one student triumphantly, referring to an article in Le Monde, a newspaper, in which the best-selling French economist argued that reducing redundancy costs will not curb unemployment.

Yet Mr Piketty was not the only rock-star French economist to opine on the labour reforms. In his own piece in Le Monde, Jean Tirole, a Nobel prize-winner, argued the opposite: that the insecurity of the young is precisely the fault of over-protected “insider” jobs. Because businesses fear being burdened with such employees, 90% of new hires are now for temporary jobs, and young people can be stuck with short-term contracts for years. The new labour law, argued Mr Tirole, should lead to more permanent hires and curb youth insecurity.

When I reviewed Piketty’s book on inequality, I pointed out that his views were surprisingly left-wing. He’s far to the left of France’s Socialist Party, and France is one of the most socialist countries in Western Europe. Even very modest and sensible market reforms are too much for Piketty.

And as far as the young people in France, don’t they realize that the current system discriminates against them?

6. (Human imperfection)X(US legal system) = $∞

FOR an inkling of how good intentions can go awry, consider Title III of the Americans with Disabilities Act (ADA). Passed by Congress in 1990 with the laudable aim of giving the disabled equal access to places of business, it has been supplemented with new Department of Justice standards (in 2010, for example, the DOJ said that miniature horses can qualify as service animals). . . .

What’s next? Omar Weaver Rosales, a Texas lawyer, has sued about 450 businesses in the past two years; more than 70% paid up to avoid a trial. But even more lucrative pastures are coming into view. In March a California judge ordered Colorado retailer Bag’n Baggage to pay $4,000 in damages and legal fees thought to exceed $100,000 because its website didn’t accommodate screen-reading software used by a blind plaintiff. Mr Rosales says extending ADA rules to websites will allow him to begin suing companies that use colour combinations problematic for the colour-blind and layouts that are confusing for people with a limited field of vision.

The DOJ is supporting a National Association of the Deaf lawsuit against Harvard for not subtitling or transcribing videos and audio files posted online. As such cases multiply, content may be taken offline. Paying an accessibility consultant to spot the bits of website coding and metadata that might trip up a blind user’s screen-reading software can cost $50,000 for a website with 100 pages. Reflecting on the implications of this, Bill Norkunas, a Florida disability-access consultant who was struck with polio as a child (and who helped Senator Ted Kennedy draft the ADA), says that removing videos that lack subtitles would deprive wheelchair users and the blind, who could at least listen to them. Mr Norkunas hopes that won’t happen, but reckons it very well might.

I’m proud to say that I’m one of the few who opposed the ADA back in 1990.

7. Who should you fear?

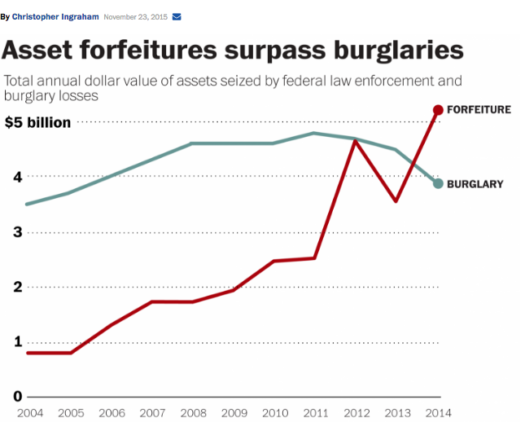

Here’s an interesting factoid about contemporary policing: In 2014, for the first time ever, law enforcement officers took more property from American citizens than burglars did. Martin Armstrong pointed this out at his blog, Armstrong Economics, last week.

Officers can take cash and property from people without convicting or even charging them with a crime — yes, really! — through the highly controversial practice known as civil asset forfeiture. Last year, according to the Institute for Justice, the Treasury and Justice departments deposited more than $5 billion into their respective asset forfeiture funds. That same year, the FBI reports that burglary losses topped out at $3.5 billion.

8. Is modern science an offshoot of economics?

In the dialectically structured thought-world of the late-thirteenth- and early-fourteenth-century universities (Latinscholae or schools, hence the adjective “scholastic”), the understanding of nature and the practice of natural science underwent profound change. A universe governed by hierarchically fixed and absolute values, Kaye argued, gave way to one characterized by change and motion. Observation and measurement displaced abstract speculation as the ways to understand nature, and that shift from deduction to quantification laid the foundations for a modern understanding of science.

That much was conventional enough. Kaye’s originality lay in his claim that the cause of this radical shift in thinking about nature was to be found in thought-patterns derived from the rapidly changing world of economics and transferred to scientific inquiry. Late medieval economic thinking was dominated by Aristotle’s discussion of value in the fifth book of his Nichomachean Ethics, where money features as the medium that makes possible comparison, measurement, and exchange between apparently unrelated things: How many shoes are equal to a house? What is the right proportion between goods and the labor that produces them?

Aristotle’s intellectual preeminence, newly restored to Europe from Arab sources, was of course foundational for the scholastic intellectual enterprise. But the rediscovery of Aristotle was not the only impetus to new thinking. In the booming mercantile economies of the thirteenth-century cities, and with the spread of the use of money, concepts rooted in the realities of the market were rapidly evolving.

Money itself was increasingly conceived as a dynamic medium connecting the constantly shifting values of commodities, labor, demand, and economic risk. The university thinkers responsible for the great shift in the understanding of the natural world, Kaye maintained, were themselves deeply immersed in this innovatory world of economics, as agents and administrators for their colleges and religious orders, and as members of the vibrant urban communities in which their universities were located. They were not only natural philosophers and theologians, but often also economic theorists and moralists, concerned with practical matters such as economic justice and especially the religious and ethical limits on usury in moneylending. And so the dynamic and shifting values of supply and demand in the marketplace, and the “monetization” of the cities, came to provide paradigms for a new and more dynamic understanding of the world as itself a dynamic realm best understood in terms of proportion, relativity, and mathematical measurement.

. . .

Kaye believes that there emerged after 1275 a novel and transformative conception of balance that revolutionized the thought of an age. A single if complex development, the emergence of “a new model of equilibrium” transformed thinking across many disciplines—economics, political theory, natural sciences, and mathematics among others—bringing to them an entirely new level of sophistication, flexibility, and explanatory power.

Food for thought.